The world is changing faster than ever before—founders and investors need to understand the implications or risk being left behind. Against a backdrop of significant economic uncertainties and political challenges, the wave of innovation led by transformational technologies hasn’t just persisted—it has accelerated. In the wake of Silicon Valley Bank’s shutdown, with headlines questioning the role and value of venture capital (VC), one fact holds true: the dependent relationship between innovation and VC—with the latter financing and enabling the founders who create the biggest and boldest solutions around the globe—fuels the engine of progress.

What will the future of VC look like amidst so much flux? As the day zero investor enabling and investing in exceptional founders across 25 locations in 17 countries—and backing them across the entire early-stage life cycle—Antler has a unique vantage point to observe shifts and trends within the VC industry. Our Future of Venture series shares perspectives on where the industry is heading through the lens of founders and investors.

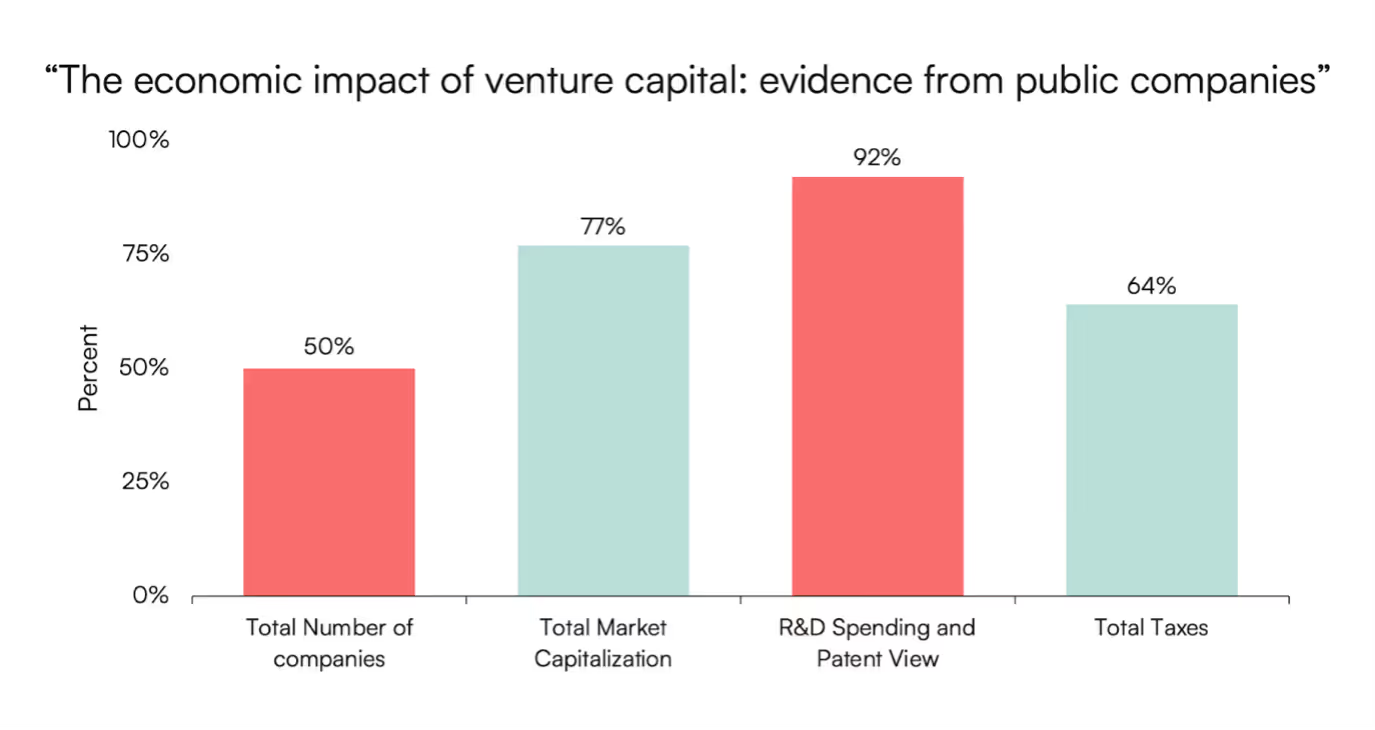

Venture capital has a much greater influence on the global economy than many realize, dating back to its modern origins in the 1950s and 1960s. As The Economist wrote last year: “VC-backed companies…make up nearly 76% of the total public-market capitalization of companies started since 1995.” In addition to employment created, venture-backed companies make up the majority of contribution to R&D spending and tax. 2021 research on US venture-backed public companies (as a percentage of all US public companies) showed the following:

These statistics underscore the role venture capital plays in creating the future. As the intersection of innovation and capital markets—charged with a culture of high growth, experimentation, and ambitious mindsets—the venture capital segment of entrepreneurship and investment portfolios is critical to society’s progress.

Today, venture is rapidly expanding far beyond America with new frontiers of innovation germinating and rapidly growing all over the world. At the same time, the sector has experienced a transformative period of funding growth over the last 10 years, with a generation of new institutional and non-institutional investors increasingly recognizing venture’s long-term role in their portfolios. There have been two main drivers:

- First, the recent sustained era of low prices, low inflation, and low interest rates supporting venture’s high growth rates (an era on which the sun has now set).

- Second, an understanding of the returns opportunities in the earliest stages of innovation exposure, amplified by the innovation megacycle in internet, data, and computing (of which we’re in the early days).

As the internet and computing revolutions gather steam across the globe—spreading into emerging middle class economies and from consumer and services to industrial economy applications—venture will be more important than ever as a lever of innovation and growth.

Venture capital has also made entrepreneurship much more accessible, enabling founders to build the most innovative and valuable companies globally. Starting off as a Silicon Valley insider game, founding a company today is a lot easier across six continents, a trend that will continue as entrepreneurs leverage knowledge and capital gained through previous tech successes. In recent years, the focus has shifted—for all the right reasons—to businesses that solve the world’s biggest problems and can yield solid financial fundamentals early in the journey.

This article, co-authored by an operator (Ronald Jan Schuurs in the Netherlands) and an investment expert (Kevin Brennan in the US), tackles two big topics:

- Will entrepreneurship be the career of choice for innovators, even in a tougher market with new financial realities, and how will venture capitalists position themselves to back the best?

- In what ways will the venture capital industry evolve—and disrupt itself—as it expands globally, professionalizes, embraces AI and data science, while VC firms compete to win and deliver more value to their portfolio companies as they adjust to new categories of investors?

Ambition to build: Five forces fueling the unstoppable entrepreneurship megatrend

Entrepreneurship has become an increasingly popular career choice in recent years—a trend that is only gathering steam with the younger generations. Why are the most talented people today more frequently choosing a much more uncertain career path over a more stable and clear road at an established company?

1. The pursuit of wealth.

The potential for greater financial rewards—partly stimulated by an increased cost of living—is causing a mass migration of human capital to innovation, with talented people starting up their own high-growth businesses. Not even two decades ago, top talent was vying to join bulge bracket investment banks and Magic Circle law firms to pursue wealth, prestige, and intellectual challenge. Today, software products turned into companies can lead to more wealth generation than almost every other pursuit of wealth, perhaps with the exception of real estate.

Seeing massive success stories in the news, in traditional media outlets and newer platforms like TechCrunch, inspires individuals to take the leap and start their own ventures, particularly in the tech industry. Three out of four entrepreneurs indicated they chose that path to “build great wealth or very high income,” according to the Global Entrepreneurship Monitor. In addition, employees are leaving big tech successes as their financial upside is plateauing. Some estimate that 70-80% of Series C and later companies are worth less than the preference stack, the money paid to investors before other shareholders (including those held by employees) get paid at an exit.

The potential reward combined with easier access to capital has triggered more entrepreneurs to start new endeavors. While entrepreneurship will never be the right choice for everyone, access to capital has become more democratized by newly organized angel groups and the institutionalization of pre-seed capital by companies such as Antler.

2. The pursuit of purpose and passion.

Entrepreneurship gives people the opportunity to pursue their passions and move away from having a job just to earn a living. Entrepreneurship creates a sense of ownership, control, purpose, and prestige. The "Great Resignation" is a phenomenon sparked by people’s search for greater job satisfaction and fulfillment. A better work-life balance is often mentioned as a reason to start “your own business,” but it is not the correct driver for founding hyper-growth tech companies.

Entrepreneurs derive a feeling of purpose by pursuing ambitions to solve meaningful problems impacting society. Addressing social responsibility concerns has become an important driver to entrepreneurship in the social context of "revolutions" such as climate change activism, social justice and equality, and the health revolution. Traditional employers—often established corporations—may not have the agility to address these topics fast enough while younger generations have embraced speed in everything they do, including: communication between people, broadcasting of news, and more. This has led to the emergence of new business models focused on ESG (environmental, social, and corporate governance) goals, which many entrepreneurs are keen to adopt as they pursue their passions.

Much of the world welcomes this trend. The 2023 Edelman Trust Barometer reveals there is a “lack of faith in societal institutions” and “business is the only institution seen as competent and ethical.” (For two years in a row, the Edelman Trust Barometer has reported business as the only trusted institution in the world.) Venture capital—even as it faces reputational issues itself—will play a decisive role in creating the businesses of tomorrow that will address society’s most pressing issues.

As more people are taking the uncertain road of starting new businesses, venture capitalists will look for ways to facilitate those journeys from day zero onwards. Many established venture capital funds, such as Greylock, Index, and Sequoia, are already moving downstream and we expect this trend to continue. An even stronger focus on and better ways to assess the grit, obsession, and skills of founders will be crucial as most company data at this stage is lacking.

3. Lower barriers to build with broadening opportunities.

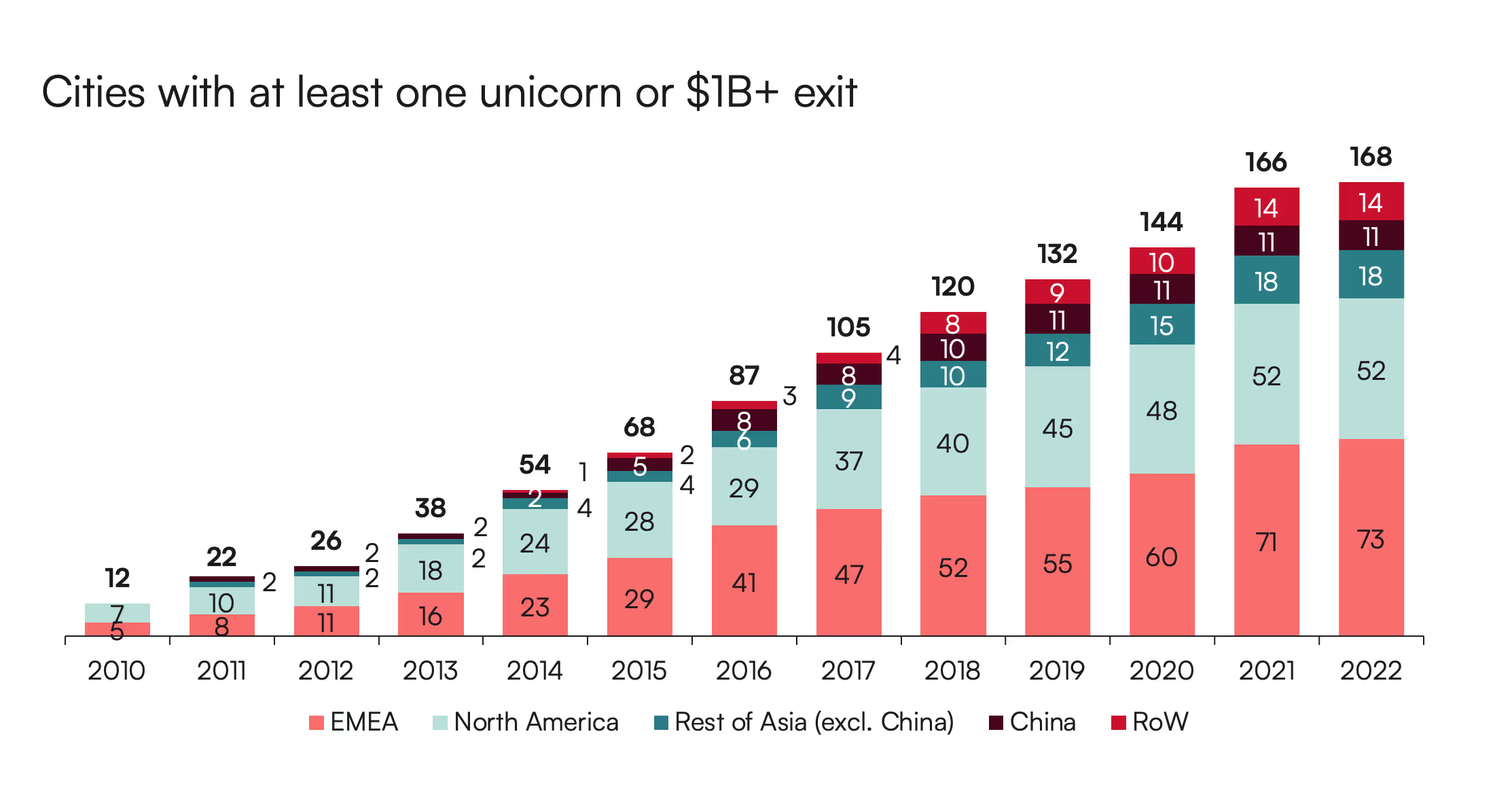

To become a successful founder today, you do not need to start your business in Silicon Valley. The “flattening” of where talent is clustering is a megatrend of the last decade that is still accelerating today. In its early history, venture-backed startups were concentrated in a small number of geographies. Silicon Valley is the birthplace of the industry and still its grandfather as a hub. And while it is still a draw for many founders, unicorn (billion-dollar venture-backed startups) home cities have proliferated exponentially in the last 10 years—from 21 in 2010, 13 of which were in the US, to 170 in 2021, with less than 25% in the US.

In the US, deals closed in every state in 2022, including Puerto Rico—an effect that is playing out in other countries at a smaller scale. As the National Venture Capital Association reports, Illinois saw the largest VC deal of 2022, and North Carolina, Pennsylvania, and Texas all ranked in the top 10.

Meanwhile, technology is much more accessible from anywhere in the world, in part due to low and no code options such as Shopify, Bubble, and MailChimp. In many cases, tech has also become a lot cheaper. You can now buy 40,000 times the storage for one-hundredth the price compared to 40 years ago. As a result, it is easier and more affordable to start a business, meaning entrepreneurs can reach a wider audience and scale their businesses faster with fewer geographic restrictions.

Entrepreneurs can pursue opportunities in large new addressable markets that are deepening globally as a wide strata of new middle-class disposable income levels flourish in emerging economies with large populations. The “Emerging 7” (E7) of Brazil, China, India, Russia, Indonesia, Mexico, and Turkey “could grow around twice as fast as advanced economies (G7) on average,” with the US potentially down to third place in the G7 ranking, according to PwC’s The World In 2050—by technology adoption spreading from consumer to business and industrial applications. As E7 markets’ growth rates accelerate, the presence of multinational corporations and high-tech business cultivated by economic development institutions form the bedrock of new venture ecosystems.

As venture capital continues to “flatten” globally, more and more countries will host unicorns with more city hubs within different countries. China, India, and the US today all have more than 10 venture ecosystems, and new hubs are opening up with new trade trends and centers of comparative advantage—for example, Monterrey on the Mexico-Texas border. VC Lab’s recent NextGen Manager Report reveals growing areas are Africa, with 14.4% of next generation firms being launched there, followed by South America at 8.3%. We expect Africa will rival funding volumes in Latin America, Southeast Asia, and MENAP (Middle East, North Africa, Pakistan) regions by the end of the decade, and Israel will continue its strength as an innovation and Middle Eastern venture capital center.

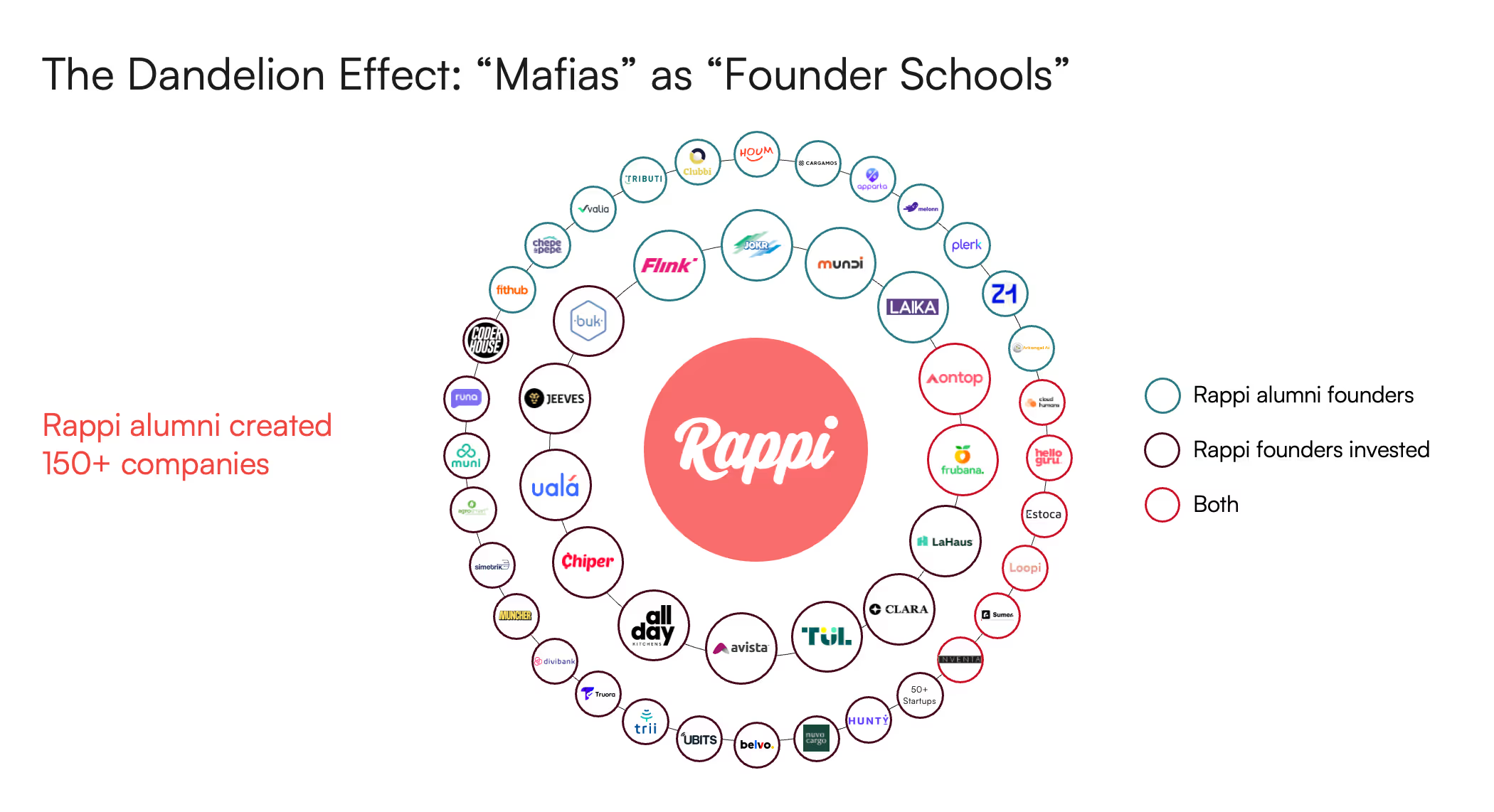

4. The “mafia effect” and innovation tribes around the globe.

Both capital and talent are more distributed as cloud and mobile computing transformed low-cost access to high-speed “getting things done.” The clustering of people who have created great companies together then bolsters real innovation in that economy exponentially by starting and investing in more new companies and forming corporate venture capital arms—for example, Alibaba Group and Bharti Enterprises.

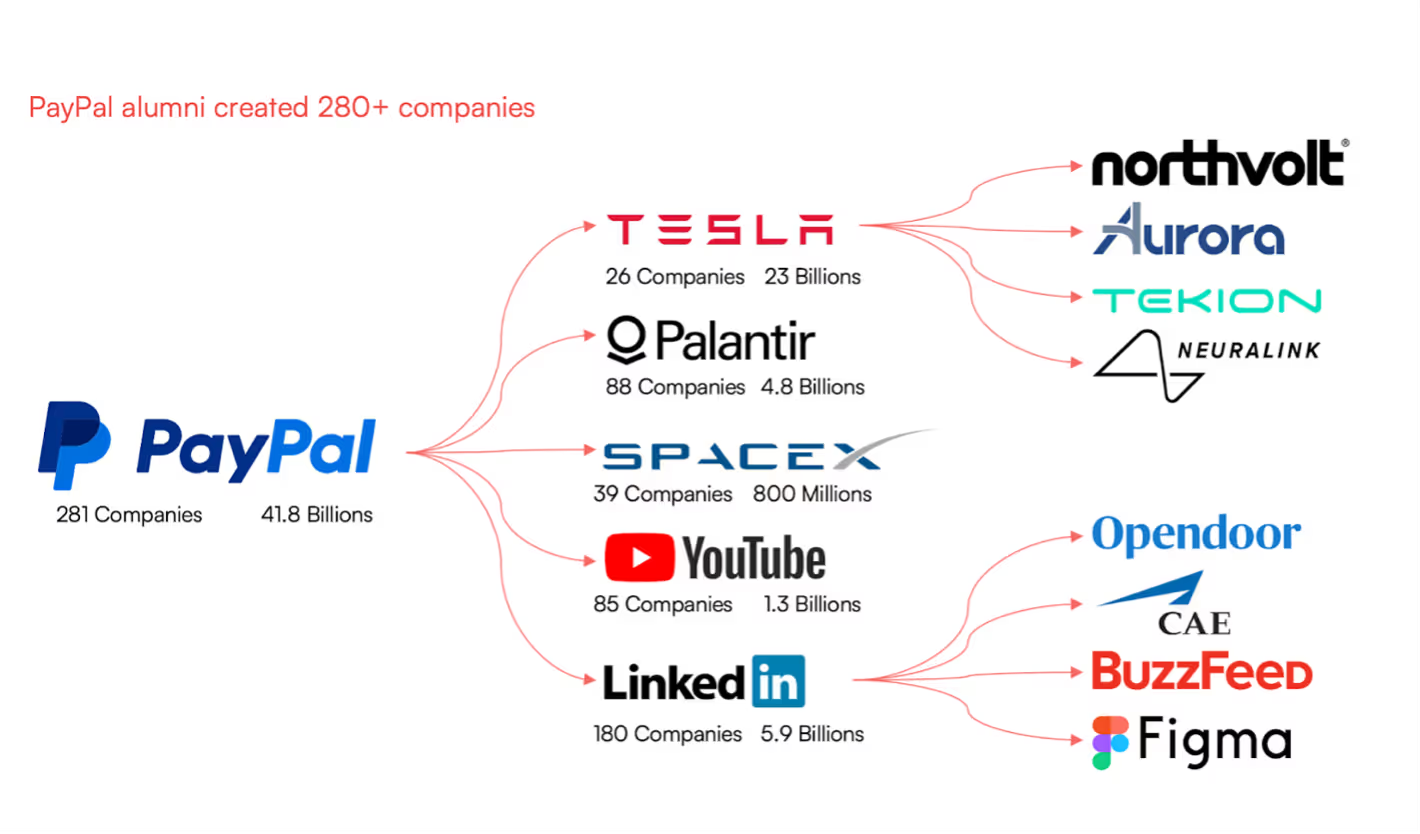

Consider the “Paypal Mafia,” the most famous group of founders that started new waves of tech successes at a massive scale (involvement with Facebook, LinkedIn, Youtube, AirBnB, Tesla, OpenAI among many others). This same generational “mafia” effect, creating tribes of innovation, is observable today in other parts of the world, with examples including Rappi (Latin America), Lazada and Grab (Southeast Asia), Rocket Internet (Europe), and Careem (Middle East). According to The Economist, “former employees of Flipkart, which Walmart bought in 2018, have gone on to found 225 startups, including five unicorns, according to Tracxn, a data provider. Those from Grab, Lazada, and Sea Group, a trio of Singaporean tech darlings, have founded or run more than 1,000 firms.”

5. Opportunities abound in the fourth industrial revolution.

New and evolving technologies continue to unlock new business opportunities. In the noughties, the invention and subsequent adoption of the iPhone or smartphone allowed all companies to thrive at an unparalleled pace—with e-commerce (Amazon, Alibaba), location-based transport (Uber, Lyft), digital marketing and advertising (Meta, Google), mobile payments (Apple Pay, PayPal), mobile gaming (Supercell, Zynga), and Internet of Things (Nest, Ring) as notable examples.

As Antler president Ed Knight describes: “The fourth industrial revolution continues to gather steam. AI, robotics, genomics, the internet of things, quantum computing, and more will be a source of immense opportunity.” With the advent of Large Language Models (LLMs) like OpenAI, companies can now analyze vast amounts of data and automate processes, creating even more opportunities for innovation. If you are able to add proprietary data components, the combination has the potential to revolutionize industries such as coding, healthcare, finance, and education, and create entirely new industries that we have yet to imagine. With Antler’s unique global footprint, we’re observing how centers of comparative advantage naturally develop—for example, the clustering of payments systems in the Netherlands, energytech in the Nordic capitals, and SaaS in India.

As entrepreneurship is changing, we believe that the asset that fuels founders—venture capital—will also see an immense shift going forward.

From “access class” to “asset class”: 11 big shifts driven by the professionalization of venture capital

At an Antler dinner with US-based investors in February, a seasoned venture investor commented that he saw VC rapidly shifting from “access class” to a more mature, professionalized asset class. With the quintupling of asset growth over the last decade, and the breadth of new types of institutional and non-institutional investors looking for venture exposure, the industry is now well beyond its cottage industry “access class” days. Specifically, the investor was referring to the industry’s professionalization, and the transparency, compliance, accounting, and business model evolutions lying ahead.

Watch for the following shifts as venture solidifies itself as an institutional asset class within private market allocations.

1. Returns to innovation sustain VC allocations.

2023 will no doubt remain sober compared to 2020-22 in venture allocations, as portfolios rebalance following the strong growth of venture in the past. Three main factors are shaping today’s investment decision-making context: growth rates needed to outstrip inflation; continuing technological innovation and the new markets for those technologies; and VC providing an embedded hedge to the risks of mature companies and sectors being disrupted. (For these reasons, Cambridge Associates recommends 40% allocation to private markets and half of this to venture capital, for growth-driven portfolios.) Driven by these factors, long-term investors will continue to support venture capital allocations though with a renewed focus on valuations and VC managers’ sources of “edge.” Experienced investors recognize the timing opportunity in deploying capital into the later stages of a downturn, as we discussed in our article “Venture investing in the downturn.”

In recent years, the increasing sophistication of portfolio optimization analysis has shed light on investors’ tendency to be less truly diversified than would be accepted in other asset classes. This results in “a cherry-picking strategy, not a diversification strategy“ as Institutional Investor stated in an analytical comment piece bluntly subtitled “three VC experts run the numbers and conclude: everyone’s doing it wrong.” Reminding us about the mathematics of power law outlier returns and how diversification reduces dispersion of expected outcomes, the authors make the important assertion that “with suitably high diversification, VC indeed becomes an investment-grade asset.”

In terms of investor types, sovereign wealth funds—often guided by their state-led prerogatives to develop innovation hubs—will continue to boost venture allocations. In addition, we already see the market expanding beyond institutional, family offices, and (ultra) high net worth individuals to include different segments of the retail market, via fractional ownership platforms (for example, SeedInvest, OurCrowd,and Moonfare). In the UK, retail investors have continued to allocate to Venture Capital Trusts in Q1 2023, given the long-term motivation for returns, and the challenges of inflation, overriding near-term market conditions.

2. VC touches more parts of the economy.

As technology and data drive change in all industries, watch for the continued broadening of the sectors and functions in which VC is playing a role. As a recent Financial Times article declared, “A new technology boom is at hand,” highlighting that three quarters of the world’s $100 trillion GDP is generated by “old economy industries” that are just starting to consider adoption of AI, robotics, and the transformative effects of advanced manufacturing. Elon Musk recently commented on this shift from the perspective of his EV supply chain concerns: “Instead of making a picture-sharing app, please refine lithium.” We already see this broadening of founders’ problem-solving interests at Antler today. For example, logisticstech and manufacturing already feature within Antler’s 792 company portfolio (as at March 31, 2023). We expect climatetech may become as large a category as fintech, an excellent example of venture capital-backed innovation being the most important route for wholesale societal problem-solving via business.

3. Shift to quality in the startup landscape.

The last year of aggressive interest rate rises will have different impacts on different business models. Settling into new higher interest rate norms is and will continue to separate the resilient from the weaker startup business models. Startups that are overcapitalized and inefficient, using leverage or with higher cash burn rates will struggle to survive. And the balance of power between investors and founders around multiples on growth rates and other valuation assumptions will be finding a new equilibrium for some time. Performance dispersion as a function of sector, vintage, and stage-focus will likely widen, and there will be disproportionate rewards for investors identifying traits of heightened market awareness and astute management skill in founders selected for investment.

4. Competition for the best potential founders.

As investors shift their focus earlier (more below), differentiation in value propositions will be the front edge of competition for the best founders—from capital, to the caliber of mentors and advisors, to the global networks that can accelerate expansion. At Antler we’re obsessed with our “founder-first” culture, and how it defines a founder’s experience building with us. Over time, this competition will result in an increased understanding of factors that maximize the probability of building great companies. Also watch for data science increasing understanding of the personality, skill set, experience, and team combination factors that have the highest probability of founder success. AI will play an increasing role in this aspect and startup business model economics, heightening the payoff to backing the right founder-idea combination. For example, we can now seriously consider this question: could an optimal use of zero code and AI support the creation of a one-person unicorn?

5. The “eclecticization” of venture—through founder backgrounds.

While the venture industry in the past has been dominated by a relatively “monocultured” (white and male) demographic, the new generation of ambitious founders is increasingly diverse. With the new problems being tackled by venture founders spanning wider global markets with deeper application across differing population demographics, watch for an acceleration in the culture of diversity in venture. In addition, the new generation of venture capitalists is a changing palette made up of ex-founders, CEOs, operators, and angels in addition to financiers. A look at the 2023 Q1 NextGen VC Managers report that surveys 401 new early-stage focused VCs offers a taste of the future. Twenty-five percent of managing partners surveyed are women and 27% of firms surveyed have mixed gender or all-women teams. In addition, managing partners with non-VC backgrounds account for 63% given the increasing prevalence of both founders backing founders, and former operators joining venture firms.

6. The “eclecticization” of venture—through specialist sector themes.

The number of managers in venture capital’s early decades was initially concentrated before the last 10 years fostered a proliferation in new managers, leading to a much more fragmented venture fund landscape. Several thousand new venture capital firms are estimated to have launched worldwide in the last five years, with boutiques positioned mostly at the seed and pre-seed stages. Over the last three years, VC Lab found that “90.3% of newly launched VCs were focused on the seed stage or earlier, picking up the opportunities left open by the established firms.” These numbers are dominated by the boutique manager and signal a wider marketplace of specialists leveraging niche expertise and networks within specific technology types (for example AI, healthtech, and manufacturing), regions (international or within countries) and themes (for example, ESG and impact, diversity). The breadth of boutique differentiation even extends to divergent business philosophies: choosing between the Hustle Fund and the Calm Company Fund for 10-year exposure to early-stage growth companies would be a fascinating decision.

7. Bifurcated markets of mega managers and boutiques.

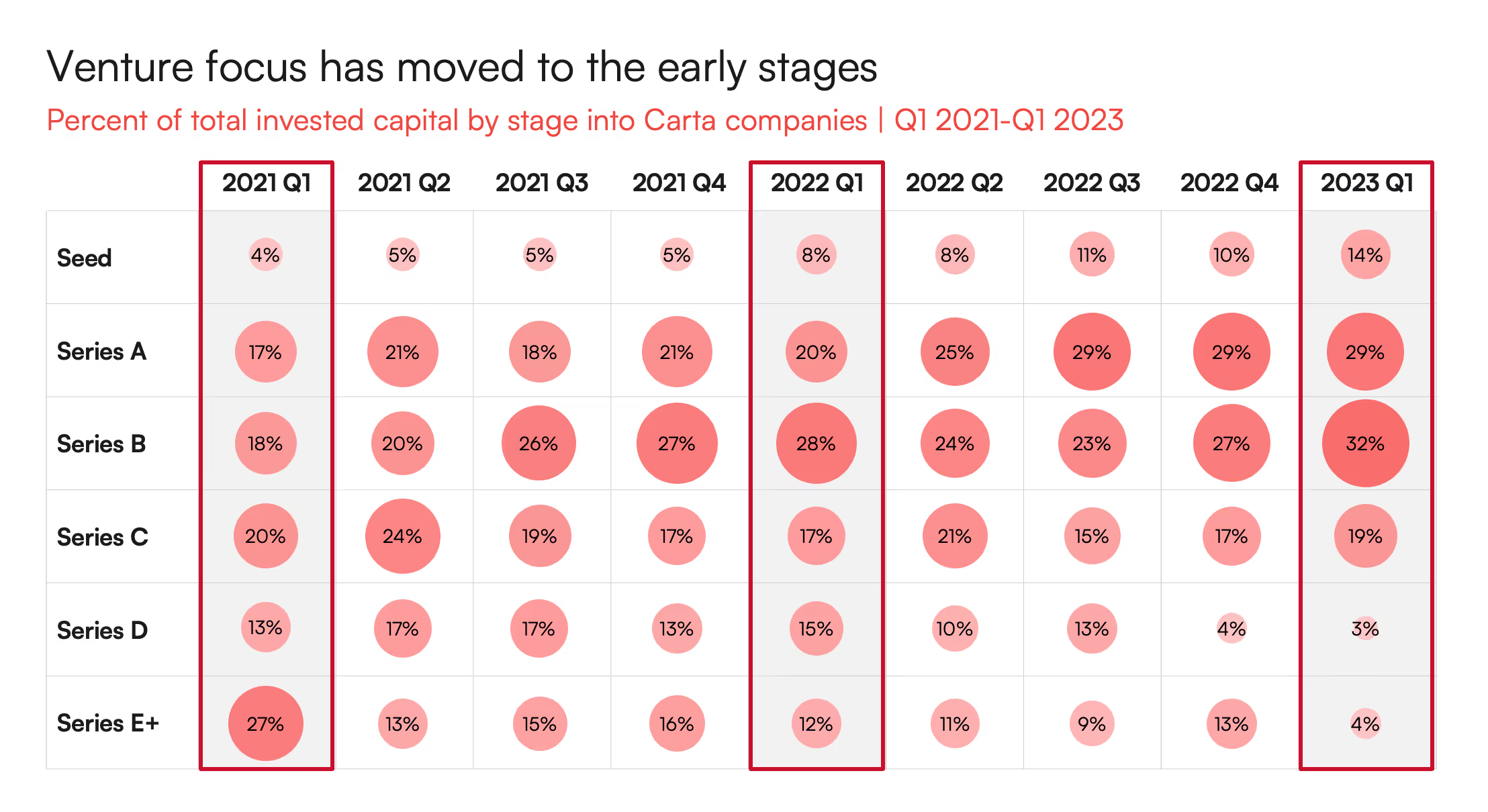

Recent years have seen a shift to increased demand for earlier stages in VC, driven by valuations and the two themes mentioned above. Proving to be less price sensitive in deploying the overhang of committed capital, pre-seed and seed valuations have been more resilient. Charting total invested capital from Q1 2021 to this last quarter, venture fund administrator Carta depicts this recent dramatic trend and the rise of the boutique manager behind it:

In the more cautious capital market environment, it remains to be seen whether the burgeoning landscape of newer managers will experience some shakeout.

At the other end of the market, watch for the concentration of mega players (over $10 billion assets under management) continuing to get larger, more corporate, and expanding vertically across stages (from seed to IPO) and horizontally in their global footprint. This “full stack” presence will be the key growth lever for them, with information and network advantages in how mega managers serve portfolio companies across different stages of funding needs. Understanding that early-stage and growth are two very different landscapes, we will likely see the mega managers partnering with experienced early-stage platforms over head-on competition.

8. Solving for liquidity.

Watch for rapid evolution of how the industry solves for early liquidity of positions. With wider investor interests in the market in terms of investment time horizon, and companies staying private for longer, there will no doubt be an increased demand for liquidity options. This will be driven by factors such as asset class ratios (venture and private equity allocation as a percentage of total portfolio) drifting from target, expressing market timing viewpoints, and venture capital managers shifting sector exposure in portfolios. The widening investor base for venture will create new buyers motivated by acquiring subsets of portfolio companies or fund tranches (exposure across full portfolio) at attractive discounts. In theory, the greater options for liquidity could enhance performance too, helping VCs keep their best performing positions for longer, especially where exit market conditions are not optimal—as is currently the case. The application of private equity funds acquiring portfolio companies via mergers (roll-ups), and strategic merger and acquisition activity (already evident according to Carta: “The number of venture-backed companies that were acquired or merged with another company increased by 20% in Q1 compared to Q4 2022, with 57% of those M&A deals valued at $10 million or less" ) will become a growing part of the exit options for early-stage funds.

9. The venture capital economic model innovates.

In a sense, it is remarkable how the 10-year fund structure and relatively unchanging fee models have sustained in an industry full of disruptors and innovators. Though there are good reasons for this, the flood of new specialist managers coming into the industry—often from backgrounds outside asset management—will surely innovate fund terms and economics to differentiate in the tougher capital raising environment, in particular to enhance GP-LP alignment.

With the long time horizon of institutional investors, “permanent capital,” evergreen structures, and continuation funds will become more and more common, with the fund sponsors offering liquidity mechanisms for those wanting to exit. And the concept of “GP commit” (partners making an investment into their fund to align with investors) will likely evolve in early-stage vehicles, where partner net worth is insufficient to place a meaningful commitment against fund size. In their business model economics, VC managers—both early or later stage—will need less capital as new technology continues to decrease costs. AI and Large Language Models (LLMs) are already being adopted in fund administration, accelerating “text in, text out” processing and communication times, and so reducing human labor. What AI will not threaten any time soon is the human relationships—so critical to deals, raising capital, and performance—that underwrite access, signaling, and trust, the nuances of which surely cannot be replaced by algorithms.

10. Competition by data.

Within the industry at an investment management level, data science is already driving the investment process and decision-making of emerging venture firms that typically develop a somewhat algorithmic approach to investment selection (for example, Correlation Ventures, Capital T, AngelList Ventures). Powered by the pace and scale of our growth at Antler, we are continually improving data analysis as a critical source of edge in our ambition to be the “day zero” partner to the world’s best founders. When you see the pace of AI language processing applied in just the last year, it feels almost impossible to forecast the speed with which “competition by data” will transform all stages of deal cycle, asset management operations, and understanding of performance and returns drivers. As Cambridge Associates wrote, “what once was considered a bingo card approach to fund construction has been replaced with a more rigorous, risk-managed assembly of companies.” Competition by data will healthily dissolve the viewpoint that venture capital is simply a matter of sufficient exposure to random outliers in portfolios.

11. VC embraces ESG factors and impact themes.

Environment, Social and Governance (ESG) management frameworks are now a norm expected by employees, customers, and investors as best practices of business management. The components of ESG frameworks are becoming more and more specific in definition and measurement with each year, shaping the understanding of business value and risk reduction. Increasingly, new venture-backed startups understand the complex expectations, value, and opportunity. A World Economic Forum survey found that 96% of startups say that ESG and impact expertise is likely to be a factor when choosing investors. ESG factors and impact-driven companies will continue to outcompete based on four key factors: opportunities in new markets through real problem-solving; winning new market share by being preferred by more and more customers and backed by more investors with capital; increasing margin and efficiency through product or service design and choice of supply chain; and superior, more diverse and transparent governance. Going forward, watch for the difference in measurement and calibration of value creation and risk reduction in ESG factors and impact-focused sectors, in particular with the increasing role of big data and AI in ESG and Impact management systems. At Antler, we have a deep-seated belief that ESG and impact will be a valuable differentiator in our business and investing approach, both as a VC and for our portfolio companies.

What’s the future of venture?

The venture capital industry has come a long way since its modern origins 70 years ago, proving essential as a driver of innovation and value creation. Despite certain aspects of the industry’s pace and growth culture in the US over the last 10 years yielding critical headlines—particularly in the wake of the Silicon Valley Bank and FTX collapses—venture capital today is in a strong position to mature as an industry while continuing to be the key driver to essential problem-solving around the world.

Looking forward, we see continued momentum of entrepreneurship as a more accessible career, technologies increasing the pace of innovation, the professionalizing of venture capital, and its relevance to more and more corners of the economy in more places across the globe. Both founder and capital markets dynamics indicate that VC is the dominant engine that will continue to fuel founders who generate solid and scalable business models in the new macroeconomic reality, which in turn will ignite further innovation.

Winners in the venture capital space will attract the most talented founders by finding better ways to analyze the probability of founder success, even before they have founded a business. Access to close to real-time data in vast amounts will be key to optimize returns. As more venture capitalists move to earlier stages and the power law potentially flattens as more startups become successful, the leading VC players will become ‘“full stack”’ and increasingly global.

In an environment of ongoing uncertainty, more investors will want to invest in the certainty of innovation—the unstoppable wave that persists through all market conditions—instead of investing only in growth, leaner operations, or enhanced capital structures. In many ways, we can think of driven founders building the biggest and boldest solutions as society’s research and development (R&D), which is as vital to the future growth of the global economy as it is to any company’s growth. Exposure to venture capital in an investment portfolio is the most direct way to fund that R&D and participate in the new era of global innovation. As the VC industry matures, sources of risk will reduce while the opportunity for long-term returns remains bright in a function so critical to global progress. As you consider your next investment dollar or career move, reflect on the question so well put by a16z’s Martin Casado: “If there’s a dollar deployed in the future, is that dollar going to fund innovation or is that dollar basically going to get predictable returns and basically stifle innovation?”

Thank you to the Antler investment team members who contributed to this article: Karl-Christian Agerup, Jeff Becker, Anders Hammarbäck, Christoph Klink, Alan Poensgen, Teddy Himler, and Saskia van den Ende.

ANTLER RESIDENCY —LAUNCH YOUR STARTUP

Antler backs exceptional founders to go further, faster.

-2.jpg)

.png)