With this goal in mind, we looked at the DACH unicorn founder landscape from the following angles:

- Unicorn founders: last year vs. this year

- All unicorn founders: top universities, employers, and investors

- All unicorn founders vs. all soonicorn founders

Why do we want to learn about great founders?

At Antler we work with founders from the earliest stage of their journey, where quantitative data is either unavailable or does not tell us much about the potential of a company. At this initial phase of a startup, investors like us rely on our own assessment of the individual founders in the co-founding team to assess potential. Given the importance of covering different areas when building a large and scalable business, it comes as no surprise that unicorns in DACH are overwhelmingly (83%) founded by teams, while only 17% have been started by solo founders.

Bringing together a strong founding team is a critical step and one of the reasons founders join one of our Antler residencies. The right team is the heart of any successful startup, and can steer the venture through the most challenging times . As we have seen in recent months, the current macro environment might prove to be one of those testing periods. The best founding teams find ways to navigate through uncertain economic conditions, access new customers, and extend their runway if they need to. Many of them will emerge even stronger from times of disruption.

An unprecedented time in unicorn-land

When we first published our DACH Unicorn Founder Roadmap, we were overwhelmed by the interest from founders, investors, corporates, and universities. The time covered in the report—from 2000 to mid-2021—was exceptional for the DACH startup ecosystem. The region saw 40 unicorn companies with 25 rising stars (the soonicorns) set to follow in their footsteps. The story was clear: DACH startups were taking the continent by storm!

Few people could have predicted what was on the horizon. Oh, what a year it has been…

In the less than 10 months since our first report was published, we have seen a record level of activity in DACH unicorn-land, including: the largest funding rounds ever, the fastest time to unicorn, and an overall record level of investments. The instant grocery delivery startups led the wave with Gorillas bagging $1 billion in its Series C round and Flink raising $750 million in its Series B round. But the q-commerce ventures were not the only ones that closed very sizable rounds at the end of 2021. Companies like N26 and Grover each collected rounds close to a billion, with the latter smashing through the unicorn sound barrier in the process.

The end of 2021 and the beginning of 2022 also saw three out of the five fastest unicorns in Europe minted—with all three companies coming from the DACH region. While Gorillas remained the startup that reached the $1 billion milestone the quickest (nine months), Flink, Razor Group, and SellerX (each 15 months) all became unicorns at a rapid pace over the last year. That means DACH startups hold the first four spots for Europe’s fastest unicorns.

The overall number of unicorns is even more impressive. While the DACH ecosystem was the birthplace of 40 unicorn companies in the period between 2000 and August 2021, in the last 10 months the unicorn group grew by 25 new members—representing almost 40% of all unicorns minted in the DACH region to date. These most recent unicorns comprise a special class—the 2022 class as we call it—so we decided to dig deeper into the band of founders behind it.

What’s new with 2022 unicorns?

When we compared this year’s unicorn class with the previous two decades, the differences we discovered were staggering.

Some of our key findings include:

- An increasing share of unicorn founders with a technical background in IT and/or software development.

- Changing founder team composition, including more teams with a business-tech skillset combination.

- Founding and/or working in a startup remain the most popular career path prior to building a unicorn.

The 2022 class of unicorns contained some of the fastest unicorns ever minted in the DACH region. However, there were also outliers at the other end of the spectrum, taking close to two decades to reach the $1 billion mark. As a result, the record-setting Flink, SellerX, and Razor Group have been offset by other outliers like the e-commerce player Chrono24 and FBA-incumbent Berlin Brands Group who became unicorns after an average of 17 years.

Another factor that could explain why the most current startup batch took slightly longer to reach unicorn status is the more prominent presence of Swiss companies. On average, Swiss startups are working on predominantly tech- and science-heavy products which take longer to develop and put onto the market. Swiss unicorns include the likes of SonarSource (cybersecurity), Roivant Sciences (health), and Climeworks (energy).

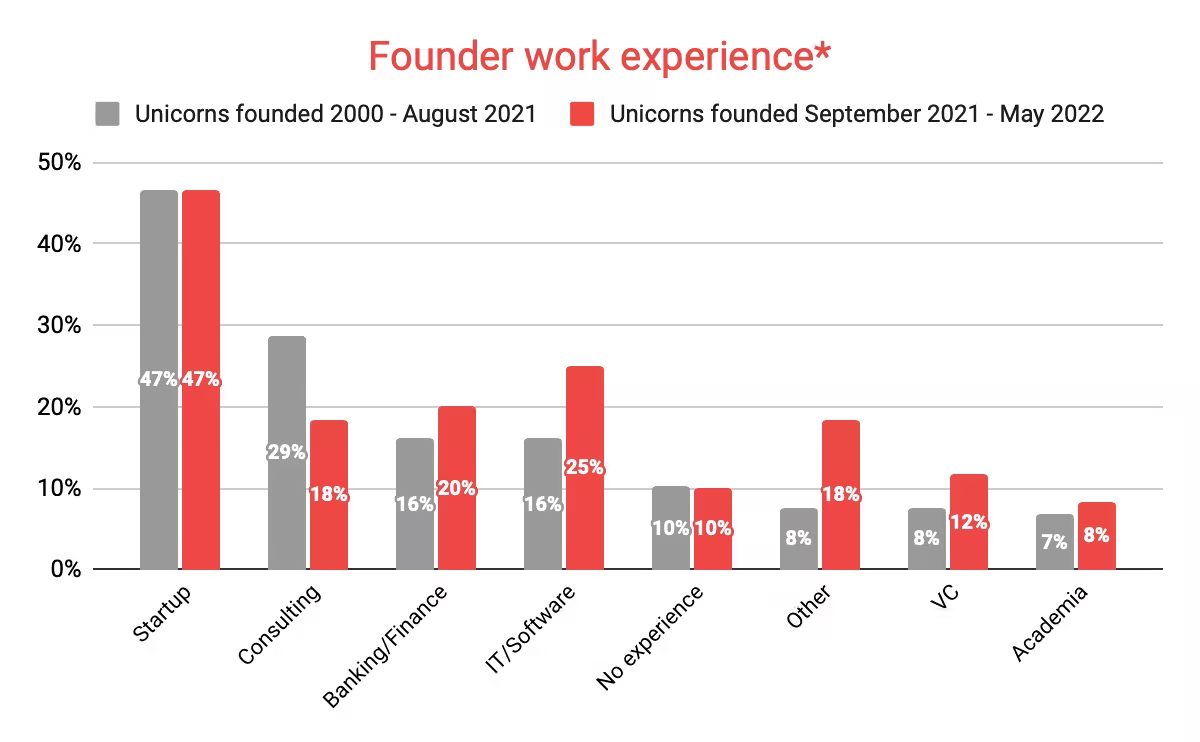

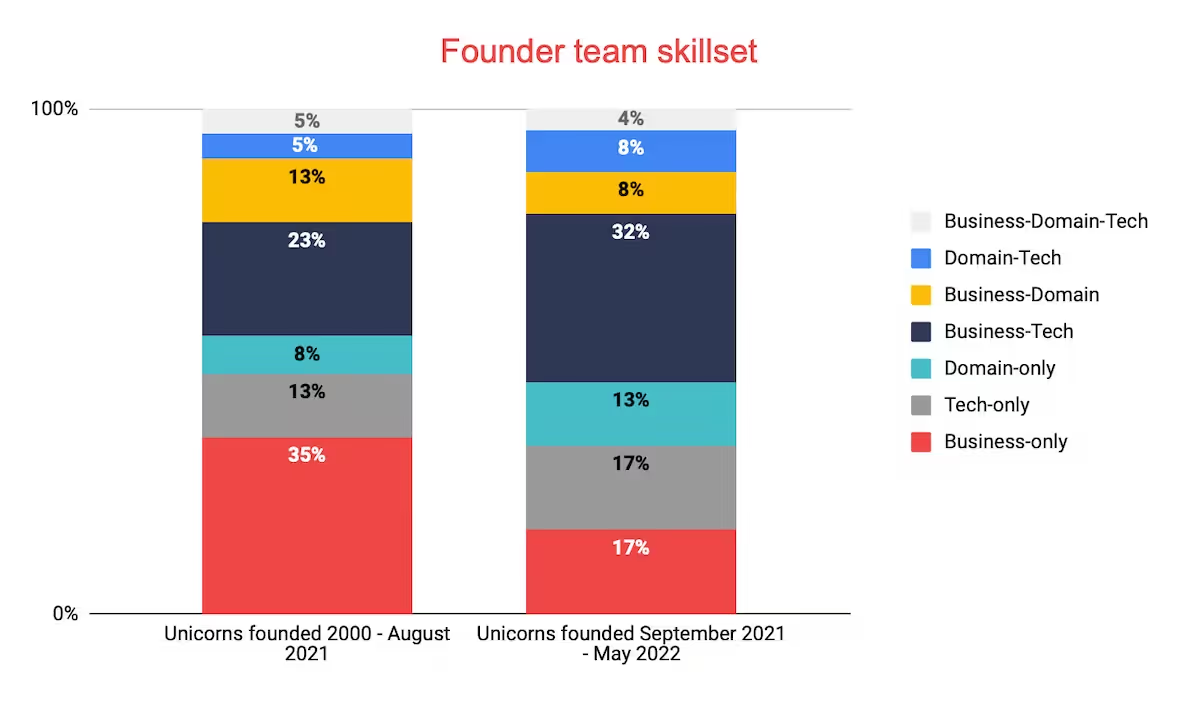

Looking into the individual founders’ skills and backgrounds, we discovered that the share of tech founders has substantially increased in the 2022 class. While previously techies comprised 26% of all founders, in the most recent unicorns 35% of founders had a technical background. This change also means the proportion of founders from a business background has decreased significantly. Of the startups covered in the 2021 report, 58% came from business experience, while in the 2022 class the proportion drops to 42% of all founders.

The boost in tech founders is also reflected in the founder teams’ skillsets within the latest unicorn class. Of the 25 unicorn teams, eight (32%) are of business-tech combination and four (16%) are tech-founders-only. This is in contrast to the past when 35% of teams consisted of founders from business-only backgrounds. Such teams are down to 16% in the 2022 class as we also see more tech-only and domain-only teams. When looking at the overall picture, business-only teams have still created the most (18) unicorn startups in the DACH region. Close on the heels are teams with a tech background founder and a business background founder, who built 17 unicorns.

We also looked at the complementarity of teams’ skillsets. In the context of this report, a team with complementary skills is composed of founders from a business and tech/domain background. We found that 48% of unicorns from the 2022 class have teams with complementary skills compared to 38% in the past. This means that while there are relatively more tech founders, they are still teaming up with founders with business backgrounds in order to successfully bring their ideas to market. Why? Because teams with complementary skills deal better with the challenges of scaling a company successfully as challenges surface on both the technical and business side. Teams with tech-only founders are less common than business-only teams. Therefore, while the percentage of business team members has decreased, there is still a need for founders with a generalist background.

Another nuance of the most recent unicorn class is the work experience they gathered prior to founding a unicorn. It is still true that most founders had startup experience, either as a founder or as an employee, before building their billion-dollar business. What’s more, the share of serial entrepreneurs among all unicorn founders remains relatively constant at 42% and 38%, respectively. All in all, having startup experience seems to be a good recipe for becoming a unicorn founder.

We also saw that fewer class of 2022 unicorn founders worked in consulting than previously. In the 2022 unicorn class, 18% had gathered consulting experience in contrast to 29% of the unicorn founders before. While the tide appears to be turning, consulting remains a fruitful career path as 25% of all unicorn founders have had some experience in consulting.

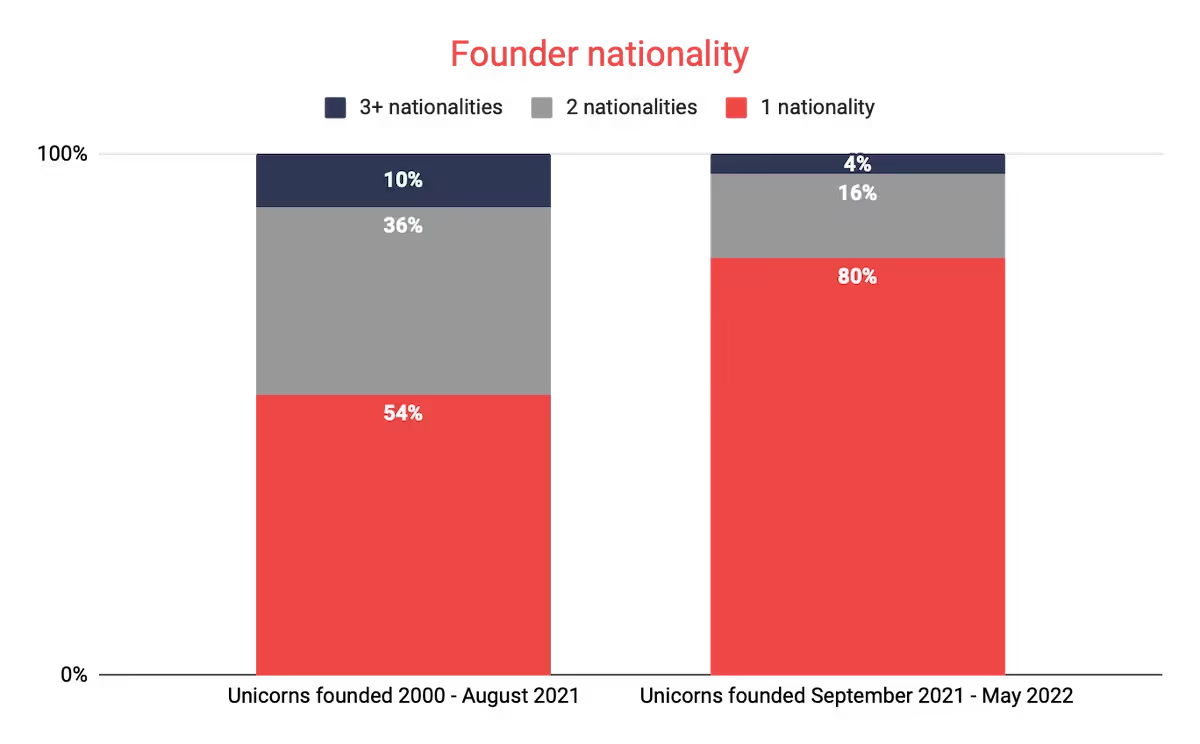

When it comes to teams’ nationality, there are interesting differences to report between this and last year. The teams consisting of founders from the same nationality have increased in relation to the number of unicorns minted. Of the unicorns built between 2000 and August 2021, 54% had teams with founders from a single nationality. In comparison, the most recent unicorn class has 80% of teams whose founders come from one nationality. Moreover, the percentage of German-only founding teams has also increased: in the 2021 report, they comprised 33% of all teams, while in the current group 48% of unicorns are founded by German-only teams.

Now that we outlined major changes in the unicorn founder roadmap on a year-to-year basis, let’s zoom out again and look at the big picture.

The 2022 Unicorn Founder Roadmap

In our new roadmap, we delved into the backgrounds of people founding the 25 new unicorns in the DACH region—looking at what they have in common, and how they differ from earlier unicorns.

The top universities of unicorn founders

Last year we observed that close to 60% of unicorn founders went to the same top 10 universities, while 47% attended the top five institutions. In addition, when considering unicorn team composition, we saw that 50% of founding teams had at least two founders who went to the same university. The more recent class of unicorn builders is attending a more diversified range of education institutions than previously, as only 30% attended the top five universities and around 45% have attended the top 10 . Overall, 42% of unicorn teams had at least two founders who went to the same university.

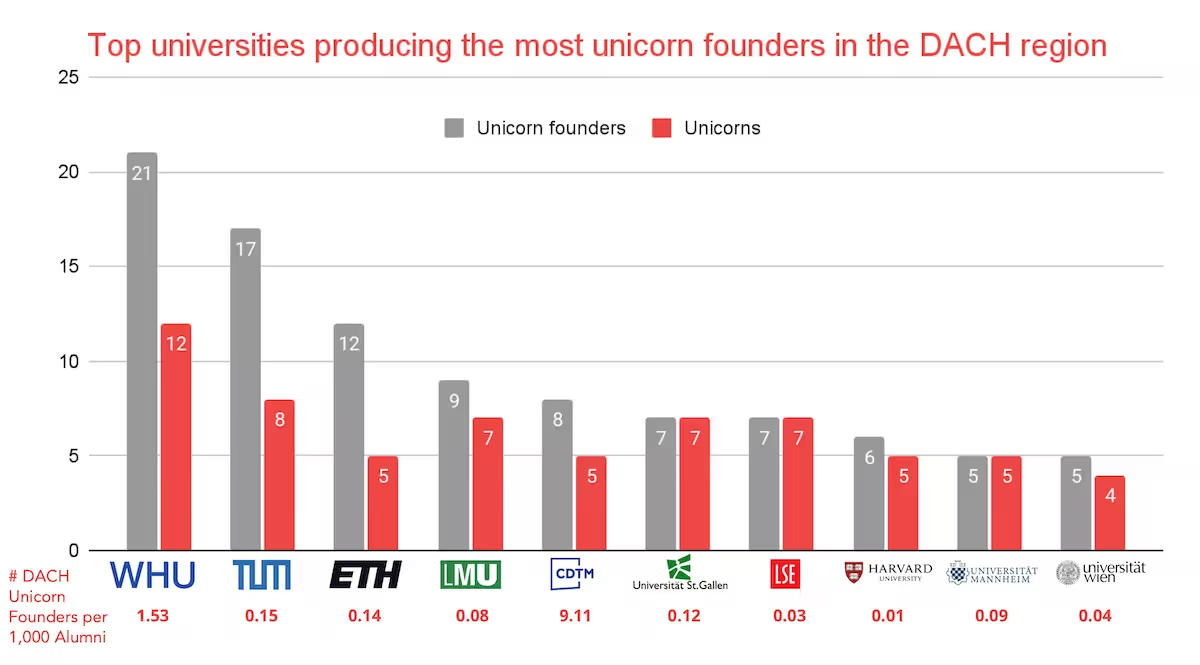

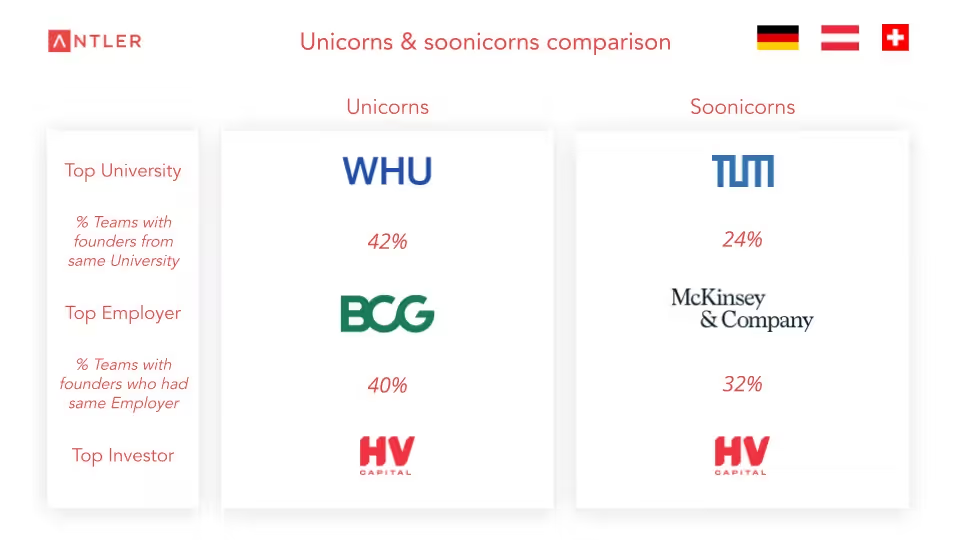

With this year’s 25 unicorn additions, the ranking of the top universities remains similar, with WHU still leading in terms of both the most unicorn founders and the most unicorns, followed by TU Munich, ETH Zurich, and Ludwig Maximilian University of Munich. University of St.Gallen and LSE share the fifth spot in the overall ranking. Interestingly, founders from ETH usually team up with each other when founding, as is also the case with founders from TUM, another technical university. A driving reason for this is that several technology companies were started by founders during their student years, and were spun off later on. Examples from TUM include Celonis and Lilium, while ETH spin-offs include GetYourGuide and Climeworks.

The new clear leader when considering the number of unicorn founders per 1,000 university alumni is Center for Digital Technology and Management (CDTM), with 9.11 unicorn founders per 1,000 alumni. The joint program of Munich-based TUM and LMU has produced five unicorns and eight unicorn founders. CDTM entered the top 10 ranking with a bang, with four new unicorns as part of the 2022 unicorn class. WHU continues to impress by producing 1.53 unicorn founders per 1,000 alumni, well ahead of the larger pack.

The top employers of unicorn founders

Between last year and this year’s reports, the percentage of unicorn founder teams that had two or more founders who worked at the same company prior to founding together has remained constant at 40%. This suggests that the first place where aspiring founders search for a co-founder is their own network of former colleagues.

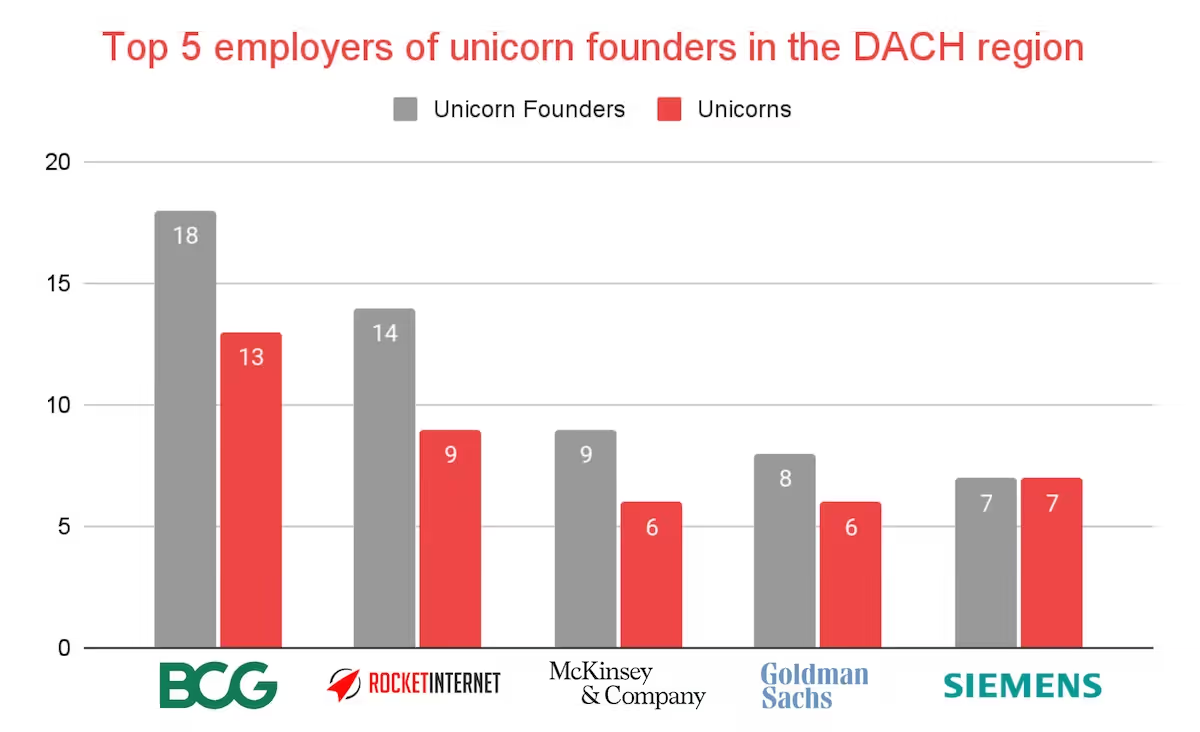

When it comes to the previous employers of unicorn founders, the top five has one new entry: Siemens. The top three remain unchanged with BCG, Rocket Internet, and McKinsey continuing to be the most frequent past career stations for founders of billion-dollar companies in the region. Also ranking again in the top five employers of unicorn founders is Goldman Sachs. The financial institution jumped up to take fourth place this year. Below is the running ranking of the top five employers of unicorn founders in the DACH region.

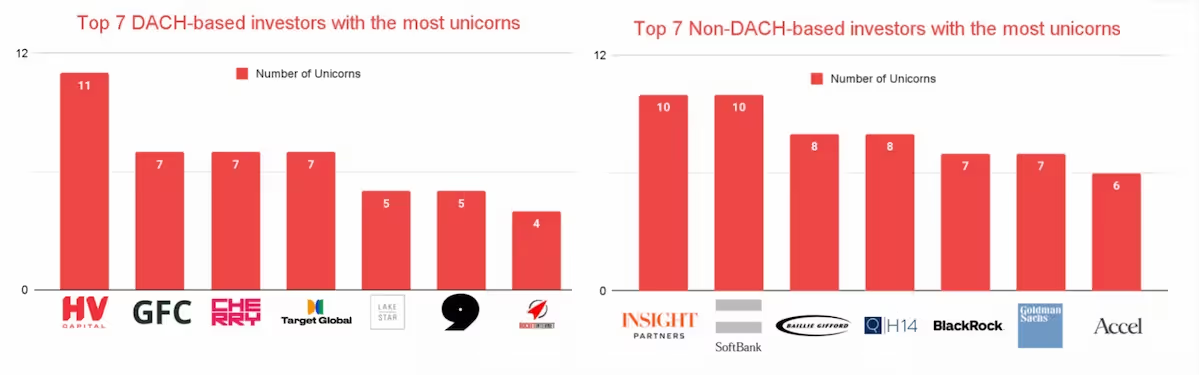

Top investors in DACH unicorns

With regards to investors, there is considerable movement in the ranking of the top investors in the DACH region. In our research we included both early-stage investors, as well as VCs who come into the later funding phases (i.e., post-Series A). We further differentiated between investors stemming from the DACH region and non-DACH-based investors.

In comparison to the 2021 unicorn class, foreign funds managed by Insight Partners and SoftBank have stepped up their footprint in DACH. Insight has invested in six of the 25 unicorns minted over the last 10 months, while SoftBank has backed five recent unicorns through various funds under its umbrella.

Strictly considering investors who stem from the DACH region, HV Capital remains on top, backing 11 unicorns. Global Founders Capital, Cherry Ventures, and Target Global all follow in the footsteps of HV, investing in seven unicorn startups each. Lakestar and Point Nine invested in five unicorns each and Rocket Internet closes the regional top-seven with four investments in unicorns. Besides the aforementioned foreign funds, other non-local investors with great track records include Baillie Gifford, H14, BlackRock, Goldman Sachs, and Accel.

The 2022 soonicorn class

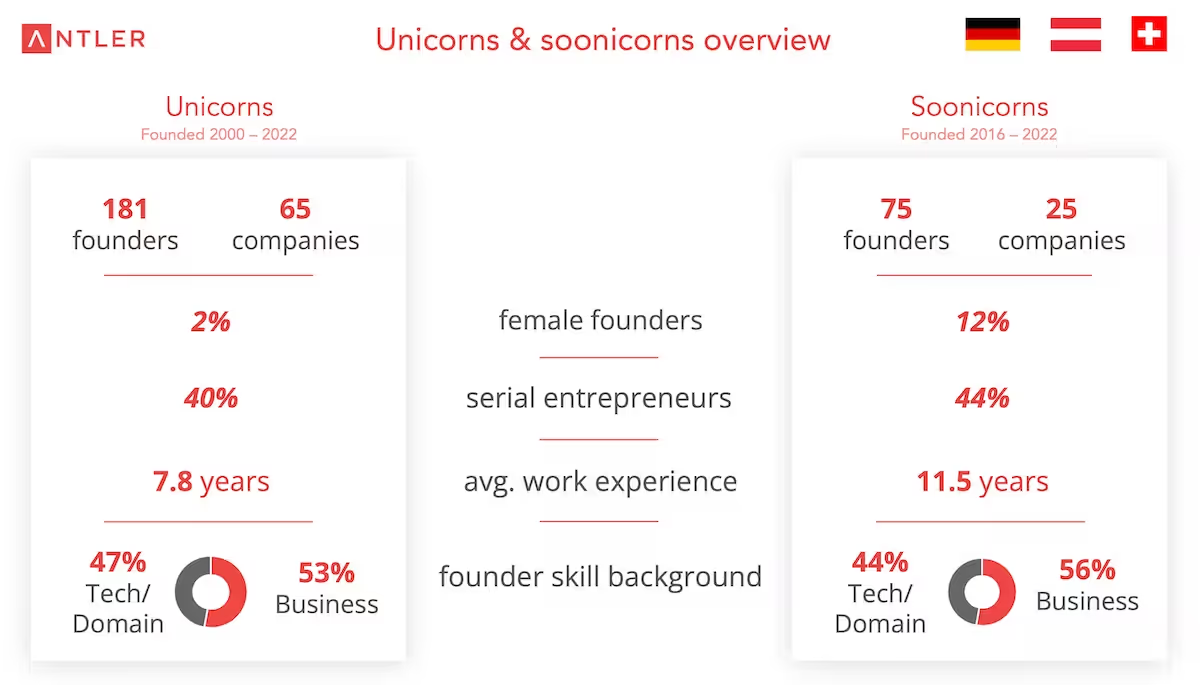

After looking at the unicorn founder landscape in detail, let’s turn to the soonicorns in the DACH region. The soonicorns—also called future unicorns—are startups founded in the last five years that have raised more than $100 million of funding and/or have a valuation of more than $300 million. This year the soonicorn list comprises 25 startups and 75 founders in total.

In comparison to the 2022 soonicorn class, last year’s report included 21 soon-to-be-unicorn companies and 60 founders. Out of these 21 soonicorn entries, eight startups have made it to this year’s unicorn list. This means that 38% of ventures crossed the one-billion-dollar mark, with four of them (Razor, SellerX, Flink, and Vivid) founded in the last two years. Below we can see the migration in and out of this year’s soonicorn list.

.avif)

How do the soonicorn founders compare to unicorn founders?

An encouraging aspect of the soonicorn founder group is its substantially greater number of female founders compared to the unicorn class. Twelve percent of soonicorn builders are women in contrast to only 2% of unicorn founders. When looking at the C-level teams of soonicorns, the share of teams including women increases to 32%; however, it is clear that the playing field is far from level.

Interestingly, when looking at founders’ nationalities, the presence of German founders is even more significant within soonicorns than unicorns. 72% of soonicorn founders are German as opposed to 58% among unicorn founders. When it comes to teams’ diversity, 72% of teams are composed of founders of the same nationality, which is higher than the 63% for unicorn teams.

Looking at the skillsets of soonicorn teams, we found some interesting differences with unicorn team skills. For example, business-only teams comprise the largest group with 40%. There are also relatively more business-domain, domain-only, and teams with founders from all three backgrounds. This change is fueled by the overall increased presence of founders with domain backgrounds. Forty-four percent of teams have domain expertise within the industry they are founding in, meaning the team has at least one founder from the domain background. This finding is considerably higher than what we observed in the unicorn team, where only 31% of teams include domain experts.

The table below shows a further comparison of unicorns and soonicorns in some of the key categories we used to analyze these startups in the DACH region. HV Capital remains the most active investor when it comes to backing unicorns and soonicorns in the DACH region. For the rising stars, we also observed that while founders do not attend the same institutions, the list of universities with the most soonicorn founders still includes WHU and LMU, followed by Heidelberg University. In terms of the top employer list for soonicorn founders, McKinsey is followed by Goldman Sachs and BCG.

What is particularly interesting is that we see a relative decrease in both the number of teams with two or more founders who went to the same university and in the number of teams with at least two founders who worked at the same company. This indicates that the ecosystem is becoming more democratized, especially for entrepreneurs who come from more modest backgrounds that do not provide an instrumental network to support them on their entrepreneurial journey.

As we observed above in the list of soon-to-be unicorns, founders are meeting their co-founders outside of universities and large corporations. In the future, as the playing field further levels, more and more founders will discover the best place to look for a co-founder is outside the box in a more diverse setting. Why? Data has consistently shown that companies led by diverse teams raise more capital and financially outperform the rest (McKinsey, 2020; Wise et al., 2022).

Nevertheless, consistent with our findings from last year’s DACH Unicorn Founder Roadmap, there is still a considerable gap when it comes to empowering founders from diverse backgrounds. Founders who are women, LGBTQ+ founders, founders of color, as well as founders stemming from less fortunate backgrounds are in need of an ecosystem that is not only more inclusive but also actively supportive.

With the launch of Antler Berlin in 2020, we are helping to build a more diverse startup ecosystem. Since then, we have supported more than 20 early-stage startups whose founding teams were formed through the Antler program. Our three cohorts in Berlin have featured founders from 29 nationalities. Furthermore, 29% of the teams we backed so far have a female founder, while 81% of teams have at least one founder of non-German nationality. Investing in diverse teams is only one of the ways in which we support the DACH ecosystem’s journey towards diversity and inclusion.

To find out more about Antler, visit antler.co and read more about the teams we have backed in Berlin and beyond. If you are an aspiring founder and would like to learn more about why founders join our residencies, read some inspiring founder stories on our Medium page. Do not hesitate to contact our team if you have any comments or questions about this report, or would like to have a chat.

The Antler team in Berlin: Alan, Christoph, Sarah, Fabian, Rafael, Yash, Gentian, Friederike, Rashko, Kai, and Nick.

Methodology

- Unicorns: Startups valued at >US$1 billion, having reached the milestone as a private company before going public or being acquired.

- Soonicorns: Startups that have raised a total of >US$100 million and/or have a valuation of >US$300 millon, and were founded in the last five years.

- Growth-stage startups: Startups that have raised >US$10 million.

- Dataset freeze: We have included data on fundraising until 31.05.2022.

- Education: For founders who have completed multiple degrees, the highest degree is recorded (i.e., MBA or PhD), while all the universities that a founder has attended have been accounted for.

- Data sources: All data were obtained through CB Insights, Crunchbase, LinkedIn, Pitchbook, and other publicly available information.

ANTLER RESIDENCY —LAUNCH YOUR STARTUP

Antler backs exceptional founders to go further, faster.

-2.jpg)

-3.jpg)