Unicorns: Africa vs. the rest of the world

.avif)

Globally, 2021 saw a record number of venture capital investments with more than $300 billion invested in the first half of the year alone and minting close to 800 Unicorns across the globe.

Meanwhile, this reality has been even more pronounced in Africa where four out of Africa’s seven Unicorns emerged in just the first nine months of 2021, and the latest US$400 million raise by Opay introduced the first US$2 billion valued African startup. By contrast, in 2015 there were no African Unicorns, and during that year, the total amount of startup venture funding was US$400 million for the entire continent according to Tech Crunch.

The continent is experiencing an increase both in volume and size of VC deals, and the number of years it takes to become a Unicorn for an African startup has reduced significantly. For example, the “oldest” Unicorns, Interswitch and Fawry, founded in 2002 and 2008 respectively, took 17 and 12 years to reach Unicorn status, while the remaining five African Unicorns took five years or less to achieve the same. The four Unicorns that emerged in Africa during 2021 took an average of 3.75 years to reach a US$1 billion valuation, one being the first Unicorn out of francophone Africa.

Who are Africa’s startup founders?

At Antler, we are on a mission to improve the world by enabling and investing in the world's most exceptional people, who aspire to build the defining companies of tomorrow. To do this, we spend hundreds of hours screening through thousands of applications, speaking to hundreds of candidates, and discovering the most exceptional individuals to join our cohorts. At Antler Nairobi only, we have received more than 8,000 applications over the past two years, and have accepted 128 founders into our four venture building cohorts. These 128 founders combined represent 30 different nationalities with 78% coming from Africa or the African Diaspora. On average, our founders have 10 years of work experience, are 34 years of age, and 25% are female.

Through this article, we aim to uncover the founder profiles behind the wider African Unicorn, Soonicorn, and growth-stage companies, and what commonalities exist between these exceptional entrepreneurs. To do so, we have leveraged our first-hand experience working closely with founders out of Nairobi and analyzed the backgrounds of the founders of the seven Unicorns, four Soonicorns, and 70 growth-stage startup founders in Africa, mainly using data from Africa: The Big Deal's latest report.

Age

We started our analysis by looking at the age of these Unicorn, Soonicorn, and growth-stage founders. Across 114 founder profiles, the median age of these entrepreneurs by the time they launched their ventures was 29, with only 20% being over 35. In contrast, the median age of Unicorn founders globally, as reported by Ali Tamaseb's Super Founders book, was 34. In addition, these founders had an average of eight years of work experience before starting their business. Only eight founders (7% of the dataset) had less than one year of experience before starting their ventures.

Going forward, it’s not difficult to believe that more African tech startup founders will start their entrepreneurial journeys early; fueled by increasing access to the internet and more startup success stories to look up to. In addition, a shortage of exciting corporate career opportunities will likely continue to drive young ambitious founders into entrepreneurship, with the potential to work on challenging problems and reap rewards far beyond what local employment could ever provide.

In all cases, through our first-hand experience at Antler, we’ve seen that experienced founders, who have a strong background in the area they are innovating in, often yield that little extra “unfair advantage” required to truly excel regardless of their age.

Origin

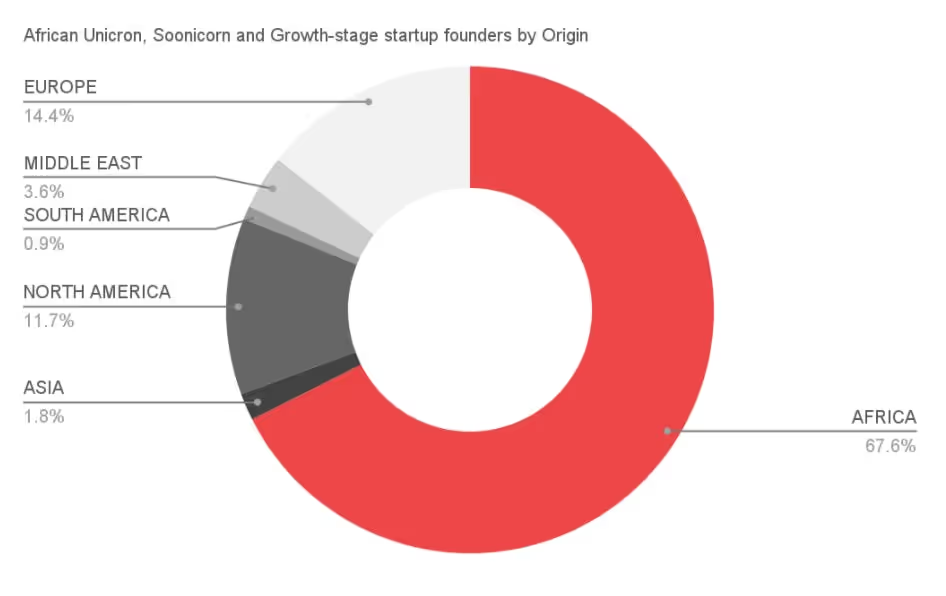

Of the total of 114 founders analyzed, 68% were African or of African origin. We also found that Egypt, Nigeria, and South Africa take the lead in producing the most Unicorn, Soonicorn, and growth-stage startup founders in Africa.

This is a particularly interesting finding in the context of a much-debated topic in various pockets of Africa as to whether a disproportionate number of local founders have historically been sidelined from early fundraising rounds. While our analysis did not delve into the distribution of fundraising success in earlier stage African startups by origin, our data for African startups that reach the growth stage and beyond shows that startups with African and founders of African origin represent the majority. This also signals that building highly scalable African startups requires deep local understanding and insight. To highlight, four out of the seven African Unicorns and three out of four African Soonicorns' CEOs are from Africa or of African origin.

Previous employment experience

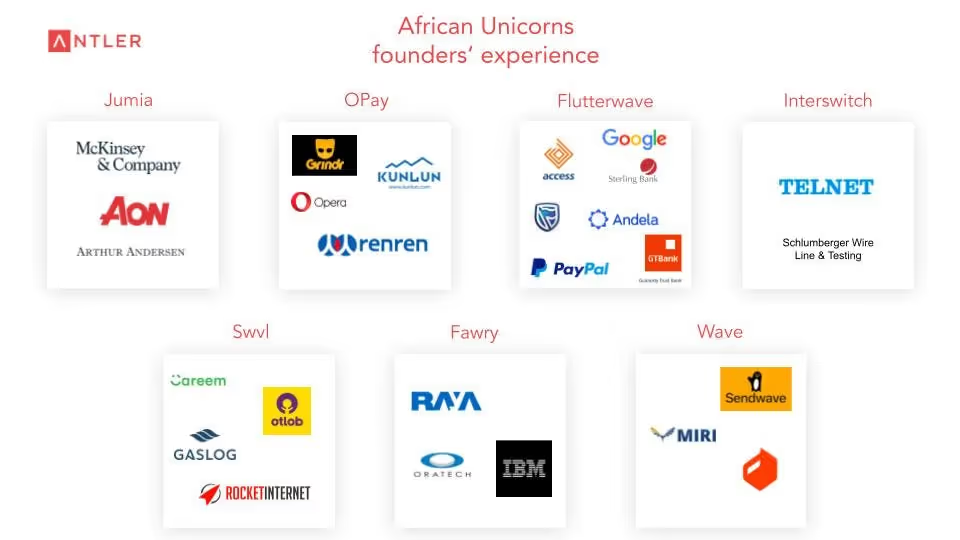

Unlike in the DACH region where five employers account for 66% of founder’s previous employment, the African Unicorn and Soonicorn founders have worked at a variety of different companies both abroad and on the continent. Our analysis shows that there is no clear dominant company where a majority of Unicorn founders have previously worked, and the majority have experience working in more than one company. Leading global tech companies such as Google and IBM, as well as high-growth startups such as Careem, PayPal, and others have emerged as previous employers of these founders. At Antler, we believe that deep industry expertise is valuable when building disruptive tech companies. In line with this, out of 12 Unicorn co-founders, 50% have previous experience or expertise in the sector in which their startups operate.

Immediately before founding their Unicorns, 25% of the founders worked at a financial institution, 17% at a consulting firm, and 42% at their own startup.

Similar to the Unicorn founders, Soonicorn founders have worked at a range of different companies both located on the continent and abroad, including consumer tech giants such as Facebook, African banks such as IBTC, and FirstBank Nigeria, and consulting companies such as Bain & Company and Roland Berger.

Unlike the Unicorn founders, only 11% of the Soonicorn founders worked for their own startup before founding a Soonicorn. Financial institutions remain well-represented employers of 22% of Soonicorn founders, while another 22% worked in the VC space immediately before founding their Soonicorn.

.avif)

Gender representation

The representation of female founders in the African tech startup scene is generally low. Of the 81 startups that have raised more than US$10 million in the past three years, only 10% had at least one female co-founder. And out of those eight companies, 80% had a female CEO, which indicates that when female founders embark on their entrepreneurial journey, they make strong leaders. Hopefully, this reality will soon change as more women join the tech startup scene and VCs start to actively and intentionally provide the space and opportunity to invest in their businesses.

.avif)

Educational backgrounds

When it comes to education, our analysis shows that African Unicorn founders attended highly ranked institutions be it at home or overseas. Unlike previous work experience that showed a diversity of companies and institutions, higher education at top schools, where founders can tap into networks both in Africa and abroad, appear to be strong predictors of success. Out of the 12 Unicorn founders, only four have received their higher-level education degrees at African Universities while the rest went to schools outside the continent.

.avif)

The story isn’t much different when it comes to Soonicorn founders’ education. Out of the nine founders, only three went to African Universities, including two at the American University of Cairo, while the remaining six went to schools in the US, UK, France, and Germany.

.avif)

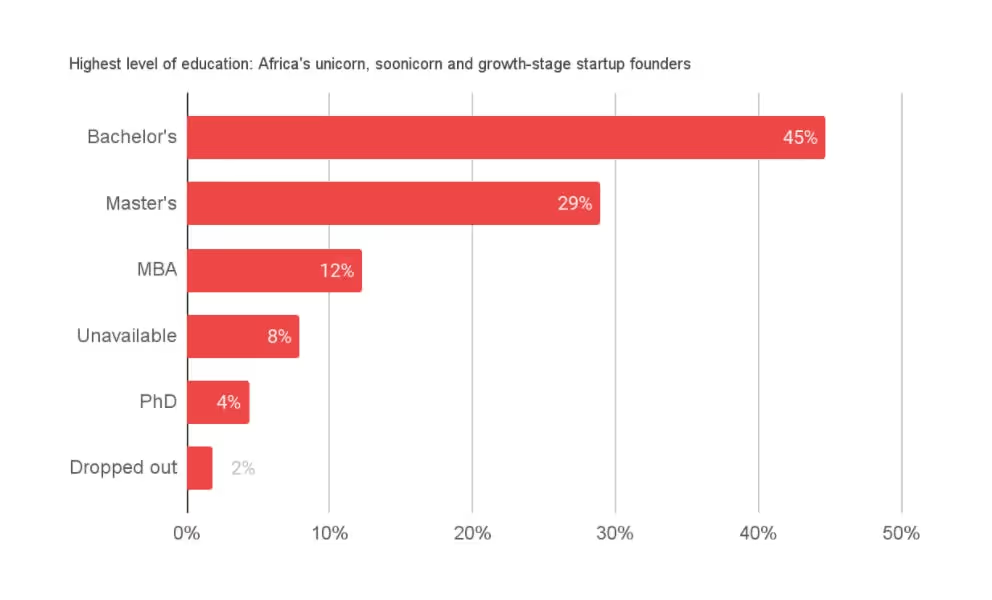

Out of the total 114 Unicorn, Soonicorn, and growth-stage founders’ data analyzed, 90% of the founders have at least one degree, 2% have dropped out and 16% have an MBA degree or higher.

The top five African universities that have produced the most number of African Unicorn, Soonicorn, and growth-stage startup founders are:

1. The American University in Cairo, Egypt (10%)

2. The University of Cape Town, South Africa (4%)

3. Stellenbosch University, South Africa (3%)

4. Babcock University, Nigeria (2%)

5. Cairo University, Egypt (2%)

While the following seven universities located outside of Africa have produced the most number of African Unicorn, Soonicorn and, growth-stage startup founders:

1. Brown University, US (4%)

2. Columbia University, US (4%)

3. Imperial College London, UK (4%)

4. Stanford University, US (4%)

5. The University of Illinois Urbana-Champaign, US (4%)

6. Harvard University, US (3%)

7. The University of Waterloo, CA (3%)

The American University of Cairo leads in producing the highest number of African Unicorn, Soonicorn, and growth-stage startup founders, but the fact that we have identified more than 100 different higher institutions attended by the founders shows that there is a significant breadth of network, diversity, and global outlook by these African founders. In addition, we expect to see more Egypt-like scenarios where leading local Universities start to produce more Unicorn & Soonicorn founders in the coming few years.

Who are Africa’s Unicorn investors?

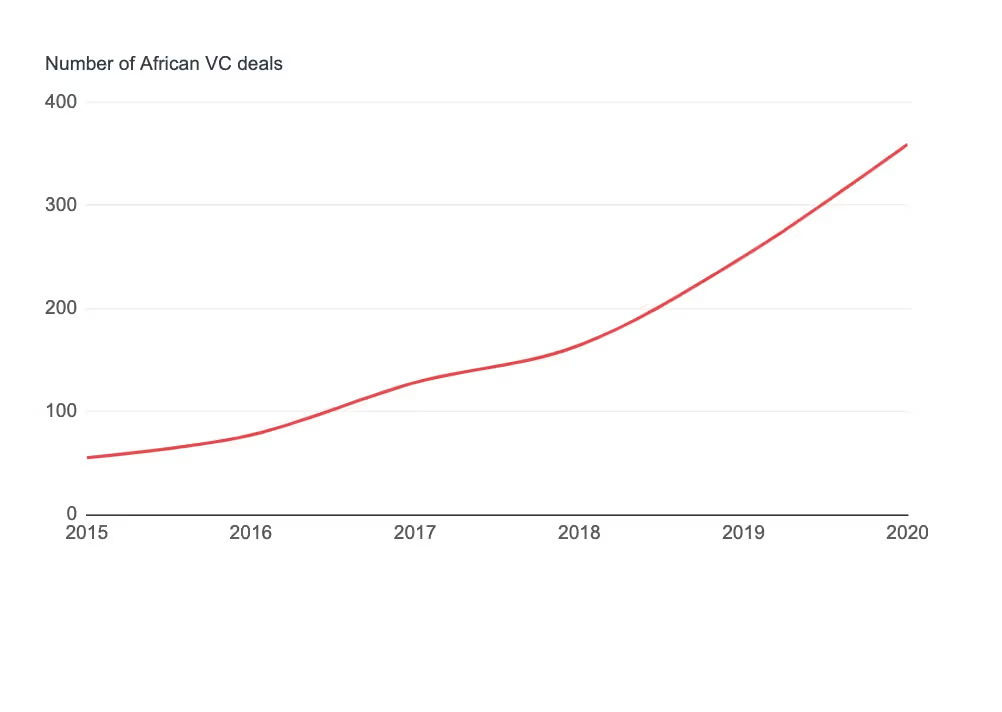

Africa, the fastest-growing continent in the world with a predicted GDP growth of 3.4% and with more than 60% of its population below the age of 25, is slowly catching up to growth led by technology and innovation. The optimism is further evidenced by the increase in the number of VC investors that are deploying funds in the continent. On average, the volume of VC deals in Africa has increased by 46% YoY since 2015, indicating growing investor confidence and willingness to take more risk on the continent.

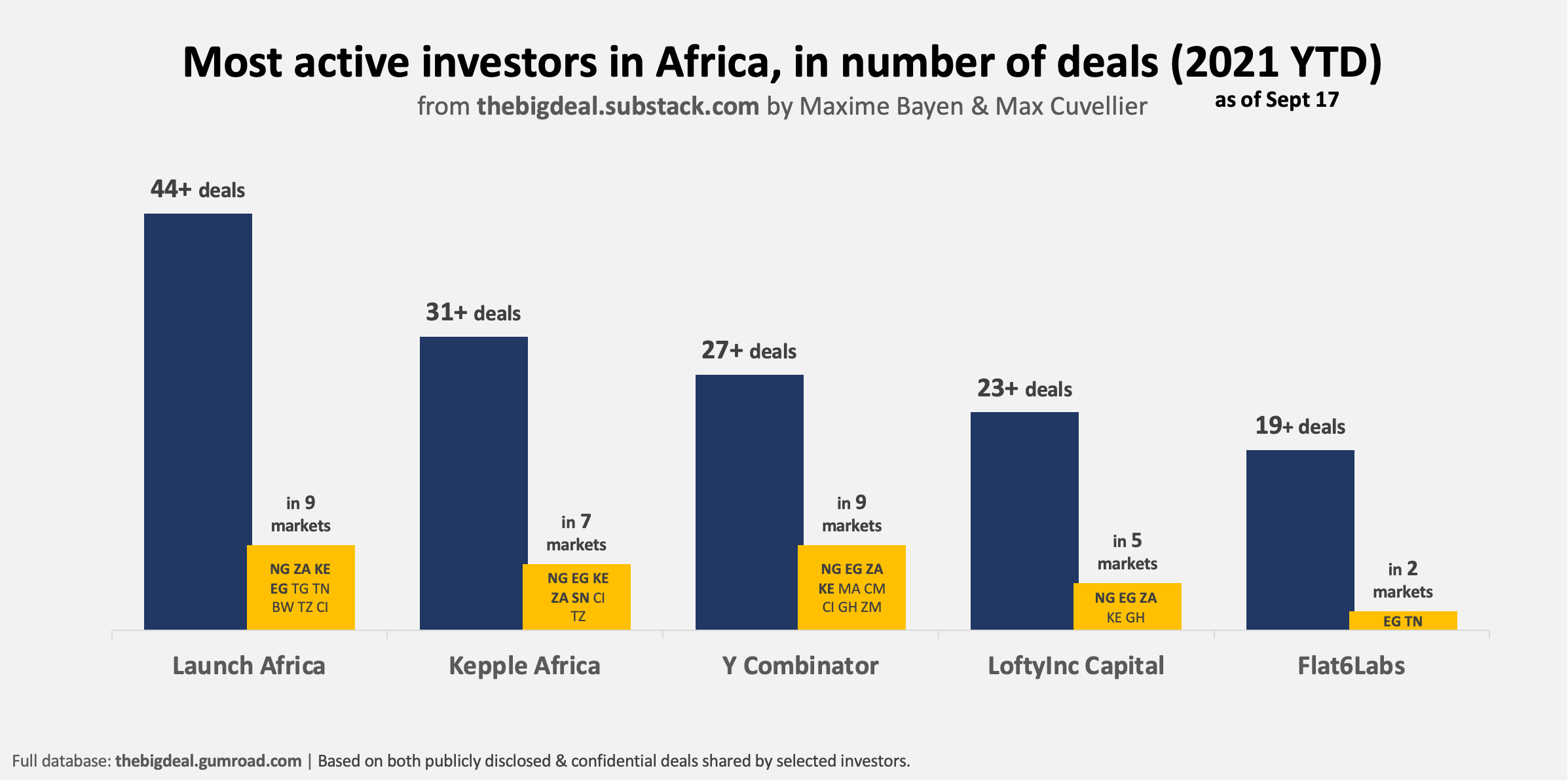

According to Crunchbase, there are currently close to 200 VC firms headquartered in Africa. So far, in 2021, Launch Africa takes the lead with the largest number of investments according to Africa: The Big Deal, while Soft Bank’s Vision fund leads the continent with the largest ticket size in a single-round investment. The majority of the later-stage investments are led by VCs from outside of the continent, while most of the early-stage deals are deployed by Africa-headquartered VCs. Soft Bank’s mega-investment in Nigeria’s Opay and Jeff Bezos’ investment in Chipper Cash are clear indicators that the larger, deep-pocketed global investment firms and angels alike are looking at Africa. We anticipate that large global VC players will continue to deploy capital where their investments can be expected to have a ripple effect across the African VC ecosystem. The coming years will likely see a transformation in the African startup ecosystem where access to capital will be less of an issue for stronger teams, fundraising rounds will be more competitive and take place at a much faster pace.

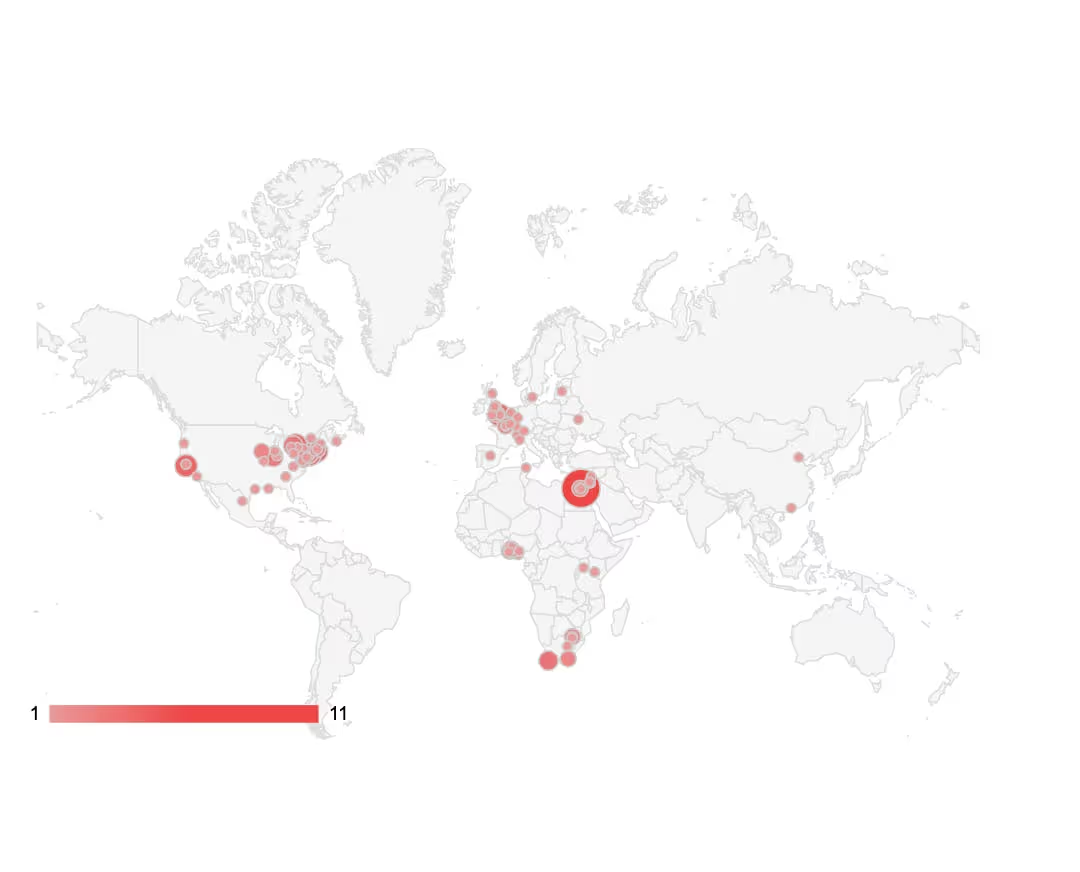

Mapping the geographic location of the top 85 lead investors in the latest rounds of funding of Africa’s Unicorn, Soonicorn, and growth-stage startups in the last three years, we observed that the continent’s startups are attracting VC money from around the world. The US takes the lead with approximately 30%, the UK follows with 15%, and Nigeria, Kenya, South Africa, and France follow the lead with each contributing 7% of the investment that has been deployed in the 81 startups analyzed. Saudi Arabia and Ireland are also found on the list as emerging players in the African VC space.

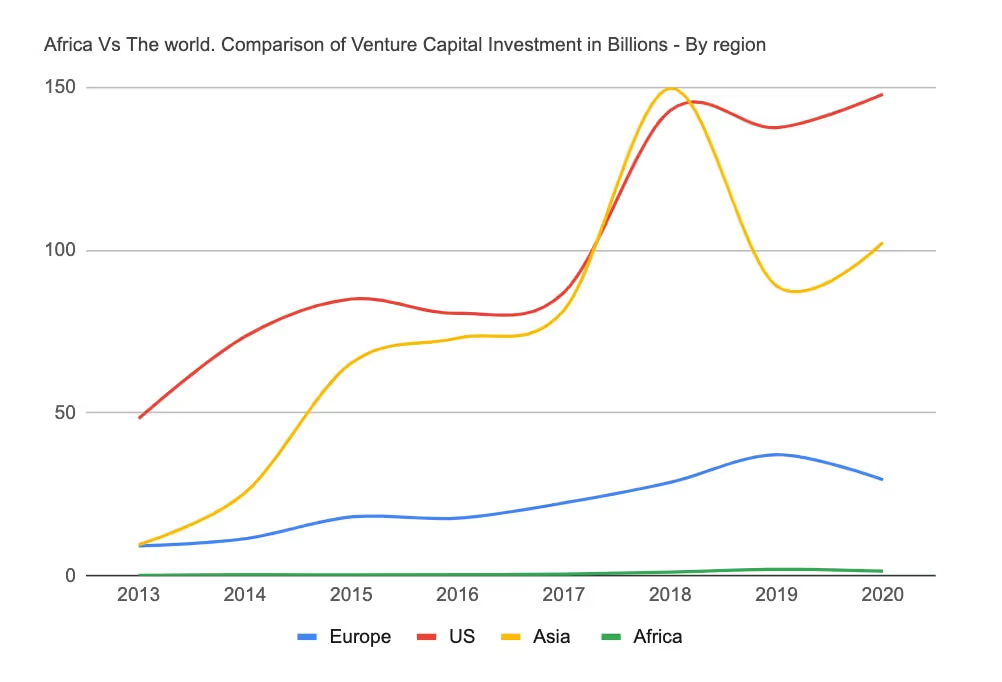

While Africa is registering record growth rates, it still lags behind other regions in aggregate capital amounts invested. Total investments in Africa in 2020 made up 3% of global VC stage investments, which makes the ecosystem still highly nascent.

In the next few years, we expect to see continuous record-breaking capital injections into startups on the continent, likely leading to several additional companies joining the African Unicorn club.

Where will the future African Unicorns come from?

From our analysis of the 81 African Unicorn, Soonicorn, and growth-stage startups we have identified that the top five sectors where these startups fall under are:

1. Fintech - 35%

2. Energy - 13%

3. Ecommerce - 12%

4. Logistics - 10%

5. Agtech - 9%

Fintech takes the crown for being the number one sector attracting the highest VC in Africa and where most African startups across the continent continue to disrupt. This is not surprising given the development level and state of infrastructure available across the continent:

.avif)

To get a sense of the future trends and opportunities, we collaborated with our friends at Ripple Research. Ripple Research specializes in using unstructured open datasets and open-source intelligence tools (OSINTs) to provide data-driven insights at scale. For this report, we analyzed over two million digital media and social media posts from January 2020 to August 2021 centered around the topic of technology and Africa.

From this unique dataset, we have found that the most popular topics are Artificial Intelligence, Machine Learning, Cybersecurity, Coding, and Software development. Conversations around emerging technologies such as blockchain, robotics, and AR are also taking place, while e-mobility related topics are slowly emerging.

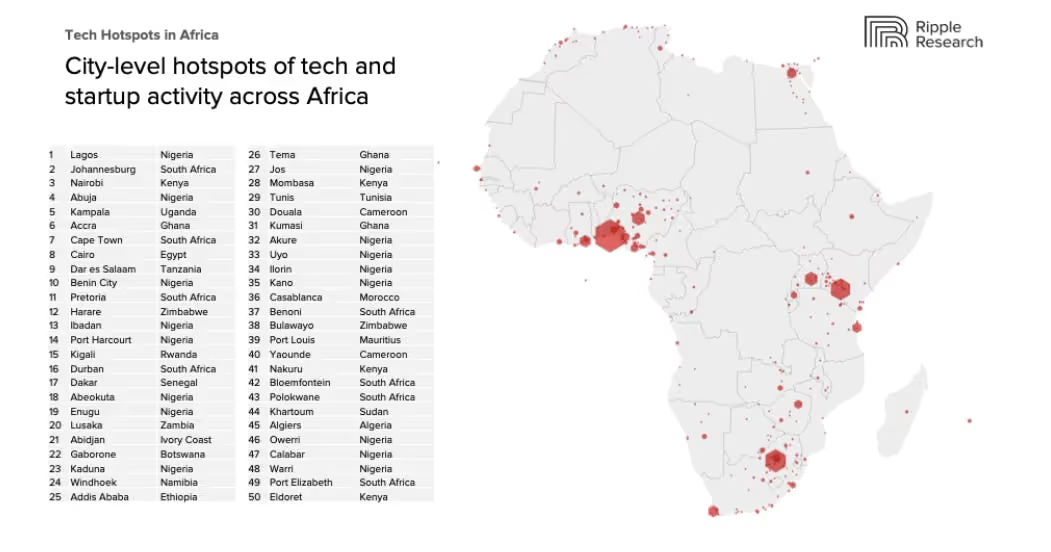

Emerging tech hubs

We further mined Ripple Research’s Africa Tech Hotspots dataset to identify startup activity with a geographical lens. Tracing where the social media conversations focusing on tech are happening gives an interesting overview of where the emerging tech hotspots are within the continent. The data shows that in addition to the known geographical tech hubs of Africa, quite a few semi-urban and second-tier cities are emerging throughout the continent.

Antler East Africa perspectives

Based on our analysis of the Unicorns, Soonicorns, and high-growth startups in Africa, their founding teams, and the ecosystem they are operating in, we believe this is a good time to launch and build tech startups in the African continent. Our belief stems from reviewing three components: founders and founding teams, investors, and industry maturity for disruption.

Founders & founding teams

Historically, Unicorn founders in other geographies have leveraged experience, skills, and networks built as employees of other Unicorns and/or tech giants to succeed in their respective markets. We believe that Unicorns and emerging Unicorns in Africa, above and beyond giving investor confidence in the continent, can also be expected to serve as hosts for developing a pool of talent capable of creating new leading tech solutions for the continent. With an increasing pool of tech talent, we also hope that in just a few years from now, outsourcing African tech development to other parts of the world could be a story of the past.

We would also expect the pioneers behind the exceptionally successful African tech startups to play an important role in the wider ecosystem, including investing, mentoring, or giving back to the next generation of local entrepreneurs, creating a positive flywheel effect. This positive flywheel effect is already being witnessed by examples such as AIyinoluwa Aboyeji and Nadayar Enegesi. These serial entrepreneurs who previously co-founded companies like Andela and Flutterwave have launched Future Africa Fund that connects investors to mission-driven startups turning Africa’s most difficult challenges into global business opportunities.

Investors

It appears that investors far and wide have taken the recent emergence of Unicorns across the continent as “proof of concept” that Africa is ripe for scalable tech investments. This growing investor confidence is reflected in the rapid increase in capital invested on the continent. A new class of investors from outside the continent who, in the past, would primarily look at later stage de-risked deals, also seem to be taking part in much earlier rounds. We’re seeing a tangible increase in earlier stage activity with some pre-seed rounds reaching double-digit million-dollar valuations, something unheard of just one or two years ago.

We also hope that the current trends will drive a “fear of missing out” among local investors to take a more aggressive role in earlier rounds with smaller tickets. Better participation from angels and local experts can boost the number and quality of upcoming African startups, as local investors have the network and know-how to mentor founders and open critical doors.

Industries & business models

We envision a bold future for African startups. As recently as a decade ago African startups used to focus on solving primarily local problems. Unicorns of today have demonstrated that it is possible to successfully roll out pan-African solutions. Going forward, as we are seeing with founders at Antler East Africa, we expect to see an increasing number of founders aiming to solve global problems out of Africa, with Africa being the launchpad.

Finally, while we envision this brighter future, we remain cognizant of the fact that there exists a divergence in innovation potential in some aspects across the continent. While certain infrastructure is keeping up with the world (e.g. mobile payments), there are obvious bottlenecks that can hold back Africa from keeping up with the trends of the rest of the world. Examples of such barriers could include education, lack of logistics infrastructure, and low consumer purchasing power, which could slow down the scalability of certain types of digital solutions or business models, such as eCommerce, AgTech, and many more.

Methodology, Definitions, and Assumptions

- Unicorns: Startups valued above US$1billion

- Soonicorns: Startups that have raised a total of > US$100 Million and were founded in the last five years

- Growth-stage Startups: Startups that have raised more than US$10 Million

- Fundraising Timeline: We have used data of startups that have raised US$10 million upwards in the last three years

- Founder age: When not publicly available, it was calculated assuming the founder went to freshman year in college at age 18

- Dataset: The data analyzed is of

undefined - For founders who have done their MBA after having had a few years of work experience prior, we have not accounted for those years as being out of employment

- Timeline to writing the article :

- We started collecting data for the article on the 1st of September 2021.

- Data collection and writing the initial framing of the article took about 2 weeks (an average of 2.5 hours of work per day).

- We did the final write-up of the article, cross-checking references and adding our insight in the 3rd week from Sept 13 - Sept17 2021.

- The article was finalized on Sept 21, 2021

- In total, the article has taken approximately 40 hours of work - Data Sources: All data were obtained through Africa: The Big Deal, Partech 2020 Africa Tech Venture Capital Report, Statista, Ripple Research, CB Insights, LinkedIn, KPMG Venture Pulse Report, and other publicly available information

This article was written by the Antler East Africa team Marie Nielsen, Melalite Ayenew, Selam A. Kebede, and Joana Borges. Feel free to contact nairobi@antler.co if you have any questions, comments, or additions to the data obtained.

ANTLER RESIDENCY —LAUNCH YOUR STARTUP

Antler backs exceptional founders to go further, faster.

-3.jpg)

{kind=link}