Done right, a VC that can offer some form of incubation incurs a competitive advantage that leads directly to better investment returns. This article looks at why incubation is so effective. Spoiler: it’s not because it helps founders be better.

That success as a VC essentially reduces to whether they end up with a unicorn in their portfolio is “VC economics 101” (and well documented). A straightforward corollary of this is that early stage VC is the craft of investing in founders who have a decent chance of creating a unicorn.

What constitutes a decent chance? Data from Pitchbook or CB Insights will show that over 99% of seeded startups never achieve unicorn status implying that any one seeded startup has a less than 1% chance of making it to that state. However, I suspect the data is tainted by survivorship bias, so the probability is likely lower.

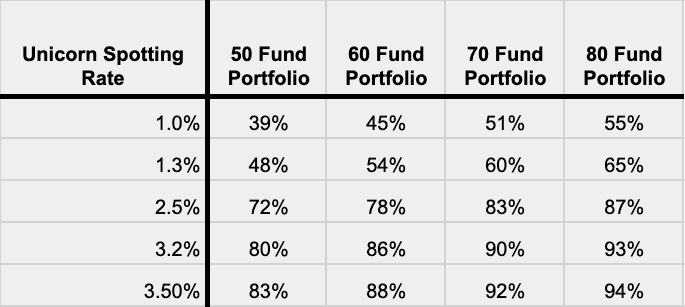

But let’s say the number is what the data suggests and the “average” seeded startup has a 1% probability of eventually exiting in unicorn territory. A bit of math1 shows that a seed stage VC with a portfolio of 60 “average” startups would probably lose money for investors. The most likely outcome (with 55% certainty) is zero unicorns.

The math affirms intuition: to be a successful early stage investor, you need the ability to invest in above average startups. But just how good do you have to be? Well, if you want the portfolio to have an 80% probability of yielding at least one unicorn, the same math will show you need to be investing in startups with unicorn probabilities above 2.5%.

Clearly, if you can build a large portfolio of high quality startups, you can have a high expectation of success.

The point here is that margins are fine. A unicorn spotting rate of 1% portends failure whereas 2.5% promises exceptionality — at least in theory. What about in reality?

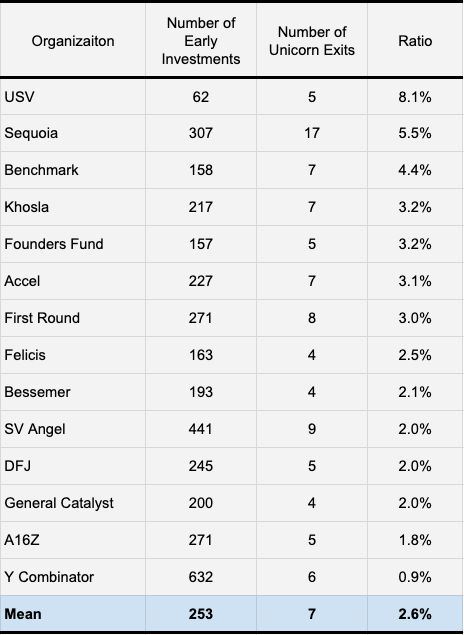

Here are the actual spotting rates of top VCs over a 15 year period:

On average, they are at 2.6% which is almost exactly what the math says must be achieved to be excellent.

How do you go from 1% (not good enough) to 2.6% (top quartile)? There are two factors that dominate a VC’s unicorn probabilities. The first is the quality of the founders they get access to; “deal flow” in the vernacular. The best founders, by definition, have a higher chance of building unicorns. If you can invest in those founders, you are necessarily increasing your portfolio’s unicorn probabilities.

Most investors compete at a disadvantage here because there are a handful of VCs who, by virtue of their brand power, essentially have a “right of first refusal” on most deals. Every VC would see their unicorn probabilities go up if they could simply get access to certain opportunities that they never see. (This is why scouting is becoming the new arena where VCs compete: the need to find and invest in great founders before they are sucked into Sequoia’s orbit is driving VCs to invest ever earlier.)

The second factor is the VC’s ability to take whatever deal flow they have and convert it to a portfolio of companies that actually have high unicorn probabilities. Actual investment skill is of course critical here. For most VCs, their success will be solely determined by just how skilled they actually are at unicorn spotting.

There are some VCs however, that do more than just try to spot unicorns. They incubate embryonic ones. The value of incubation to a founder is well understood: they get infrastructure, coaching, access to domain experts, pathways to customers, etc. It’s real value and can be impactful.

One might think the value to the VC is the same thing: by helping their founders they make their portfolio better. This is technically correct, but only to an extent. No incubator transforms a flawed startup into a unicorn.

The actual value of incubation to a VC is data. An incubator is actually a laboratory that produces observations about a founder’s abilities. Can they move fast? Can they communicate? Can they build? Can they sell? Incubators yield answers to the essential questions every early stage investor is trying to answer.

Where a traditional investor tries to answer these questions through a series of meetings with founders, the incubating investor gets the answers from observations. Importantly, they get these answers with a level of certainty that is simply impossible to achieve if you are limited to traditional diligence methods.

This is the competitive advantage that incubating early stage investors have versus traditional investors. When done well, it increases unicorn probabilities materially. I’ll use Antler’s incubation-like model and some data to quantify just how big this advantage is.

First let’s create a baseline. To do that, I’ll reach to this simple CB Insights dataset for the analysis. The dataset tracked 1119 startups from seed investment to their ultimate end, tracking survival rates and outcomes. Of those, 15 (1.3%) exited as unicorns.

I don’t know if the investment decisions of an average VC achieve better or worse survivorship statistics than what this dataset implies. But it doesn’t matter. I just want a baseline to study what happens when you introduce incubation into the investment process.

There are two key measures I’ll take from this data. The first is the initial “seed graduation rate”; i.e. what fraction of seeded startups manage to raise another round. That number is 48%. (Of 1119 companies, 534 achieved a subsequent funding round.) The second is the unicorn probability given the fund graduated from seed stage. That number is 2.8%. (Of 534 companies that raised again after a seed round, 15 exited as unicorns.)

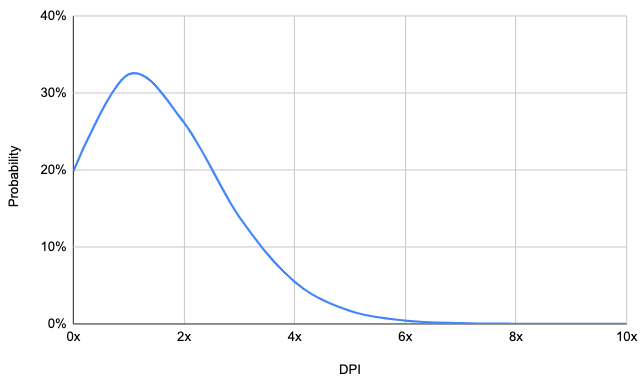

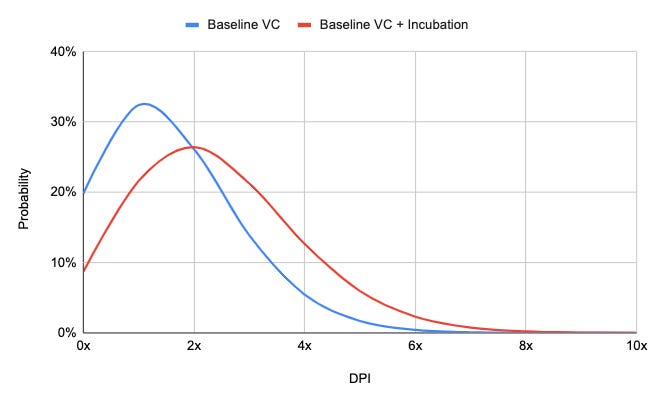

So consider now our baseline, a hypothetical VC that can achieve these survivorship rates. This VC is seeing 48% of the companies they seed graduating to additional funding. Each of those has a 2.8% of a unicorn exit. So every investment they make has a 1.3% unicorn probability. If they seed 80 companies over the lifetime of the fund their expected DPI is 1.6 with a DPI density that looks like this:

Now let’s say you now give this same VC the power of incubation in the way a firm like Antler does it, which is basically:

- Identify promising founders.

- Host them for some months giving them resources and support but also intently studying everything they do.

- Use the learnings from step 2 to seed a subset of hosted founders.

Obviously this is an oversimplification, but it captures the essence of the system. Notice that step 1 is not much different from the process any good early stage VC would run: meet founders, listen to pitches, follow up with the better ones, filter out the rest. From here, for most angels and early stage VCs, the next step is investment.

But in Antler’s model, the next step is incubation – “residency” in their words . Founders start or continue building their business leveraging Antler’s infrastructure, resources and support. Over the subsequent months, as one would expect, some founders do well; others don’t. This is the “data” that incubation yields.

This data contains information you cannot get any other way; there is no amount of time you can spend talking to a founder or diligencing them in some other way that can match what you can get from watching them operate. The result is that Antler can pre-identify many of the startups that would likely not graduate to a second round of funding.

What is the actual effect of this on expected fund performance? Returning to our hypothetical VC: The baseline seed graduation rate is 48%. That means about half of their seed investments they make never raise again.

Then introduce incubation. The VC now has data that identifies their future failed investments before they have written a check! Even if incubation only identifies a third of the future failures, the seed graduation rate goes from 48% to 62%. If it also happens to identify a few founders that don’t pitch well but execute superbly, the number gets even higher.

When the seed graduation rate goes from 48% to 62%, the VC’s overall unicorn probabilities go from the baseline of 1.3% to 1.8%. That has a massive impact on expected performance. Expected DPI goes to 2.6 and the entire density function shifts right:

Incubation in the Real World

The data I have on the impact of incubation comes from Antler and it’s not difficult to interpret. Since 2019, Antler has made 1507 investments in early stage startups. Of those, 61% (919) went on to raise additional funding. In other words, their seed graduation rate is 61% which is way above the industry average that the CB Insights data implies.

Now granted, Antler is very experienced at executing their version of incubation, so this data probably represents “best-practice” incubation and not the industry average, but it nonetheless is entirely consistent with what theory suggests should happen.

Two Caveats

While theory and empirical evidence makes a very strong case for the power of incubation, there are two important caveats.

Firstly, incubation is a competitive advantage not a panacea. A seed investor lacking the myriad skills and resources success demands, cannot ascend to excellence just by adding incubation. Executed well it will help but it can’t compensate for lack of core expertise.

Secondly, there is not some switch you flip that converts your VC operation into an incubator. Doing incubation effectively demands a certain set of skills and abilities different from what traditional VC requires. So yes, incubation is a potent advantage for a VC but it has its own barriers to entry.

So, no matter how good an early stage VC’s core investment skills are they can improve their outcomes if they can do incubation well. Building an incubating VC or transforming into one is not an easy task, but the ROI is there for those who can.

ANTLER RESIDENCY —LAUNCH YOUR STARTUP

Antler backs exceptional founders to go further, faster.

.png)

.png)