.avif)

This article is co-authored with Mathias Owing Maanum and Emma Parker. Together, we explore:

- The areas most ripe for disruption

- New monetization models needed for agentic systems

- The infrastructure deep dive: 50+ startups building in the space

- Our three lessons learned for investors and builders

Commerce has always been a dance between what people want and how fast the world can deliver it. For decades the bottleneck wasn’t demand, it was brains. Buying decisions, price checks, supplier searches, invoice matching, contract terms, all of it required humans in the loop. Human time is slow, expensive, and frustratingly finite.

Then something happened. Agents got smart. Reasoning models became good enough to make decisions rather than just autocomplete sentences. They remember context, follow goals, plan, monitor, and correct. Tools arrived that let agents browse the web, query databases, call APIs, read emails, and execute actions. Costs dropped. Behaviour became reliable. A threshold was crossed: agents stopped being toys and started becoming co-workers.

Agentic commerce has emerged as a new form of shopping where AI agents execute transactions on behalf of users, businesses, or themselves.

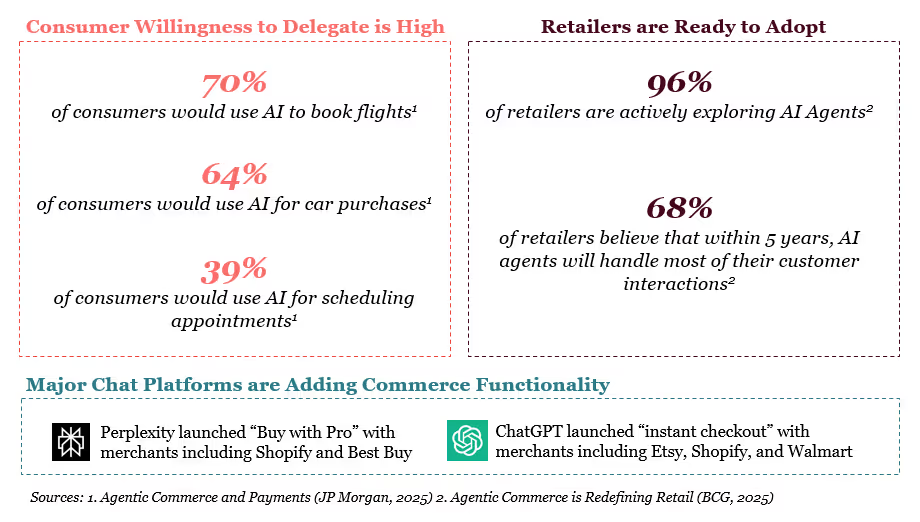

Demand has erupted, and the agent economy is expected to explode. AI traffic is up 4,700% YoY (BCG, 2025). Agentic commerce could generate up to $1 trillion in orchestrated retail revenue by 2030 in the US alone, and $3-$5 trillion globally by 2030 (Mckinsey 2025). 85% of procurement leaders (Digital Commerce 360, 2025) are deploying agents. Yet, whether this demand fully translates into a functioning agent economy remains an open question. We're only just beginning to move from product discovery assistance today, to purchase-in-chat, to a future state of fully autonomous agents and ultimately to agent-to-agent commerce. The opportunity is real and accelerating, but realizing it depends on agents becoming reliable, trusted, and economically viable at scale, a bar the ecosystem has not yet cleared.

Hot Spots of Demand and Areas Ripe for Disruption

Agentic commerce represents a fundamental shift in how transactions occur online, encompassing workflows where AI agents execute transactions on behalf of users, businesses, or themselves. But this shift is unfolding across two very different types of transaction flows.

The first involves agents operating within existing consumer and enterprise workflows, such as retail purchases, travel booking, or B2B procurement. The second introduces fundamentally new transaction flows, where agents pay for AI services, often at a sub-cent scale. Distinguishing between these two categories is critical, as they differ meaningfully in adoption dynamics, infrastructure requirements, and monetization models

Consumer commerce

Consumer commerce is entering a new phase as AI agents move from assisting discovery to executing transactions end-to-end on behalf of users. Today, consumers are already using generative AI to search, compare, and shortlist products, and the impact on retail traffic is material: visits from GenAI browsers and chat services surged 4,700% year-over-year by mid-2025 (BCG, 2025). Crucially, this is not low-intent traffic. AI-driven shoppers spend 32% more time on site, browse 10%+ more pages, and show 27% lower bounce rates (BCG, 2025). They arrive further along the purchase journey, having already refined preferences and compared options in ChatGPT or Perplexity before reaching merchant sites.

The natural next step is to close the loop and transact directly within these environments, collapsing the traditional funnel from search to checkout into a single conversational flow.

Consumer interest and platform development is most advanced in verticals where discovery is already taking place on chat platforms, particularly travel and fashion. Across both verticals, checkout remains largely manual today, but momentum is clearly moving agents from discovery toward execution.

- Travel: startups such as Layla, Mindtrip, and Wanderboat deploy agents that plan itineraries, search across airlines and hotels, compare prices, and generate personalized recommendations. While most experiences still redirect users to partner sites for checkout, agents already surface live pricing and availability, pointing toward a future of fully autonomous, multi-leg booking and in-chat transactions.

- Fashion: platforms like Alta, Daydream, Doji, and Look.ai use natural-language search and AI-generated imagery to help users articulate intent and visualize complete outfits with real, purchasable products. Because fashion is inherently visual, these tools drive higher engagement and an estimated 7% lift in average order value through personalization (Agentic Commerce and Payments, JP Morgan, 2025).

B2B Workflows

Controlled environments, clear ROI, and higher tolerance for operational risk are driving deployments in B2B use cases. Enterprise workflows operate within predefined spending limits, approval structures, and compliance frameworks.

Early traction is concentrated in core financial workflows.

- Procurement: Deploy agents to automate catalogue navigation, negotiate pricing, approvals, and vendor management. Adoption is already well underway: 85% of procurement leaders are piloting or using AI, with 73% actively deploying agents, reflecting strong pull from teams under pressure to reduce cycle times and manual overhead (Digital Commerce 360, 2025). Startups include Omnea, Magnetic , Levelpath, Zip, Didero.

- Accounts Payable: Vendors are automating invoice ingestion, approval routing, and payment execution, reducing reconciliation work and accelerating cash flow; 40% of AP leaders plan to adopt agentic systems within the next year (Saliotech, 2025). Startups include Natural.

- Payroll: Represents one of the clearest ROI cases, enabling autonomous disbursements and regulatory adjustments within defined parameters, delivering cycle-time reductions of up to 35% (KPMG, 2025).Startups include Niurial and Central.

At the same time, enterprise adoption is constrained by the realities of legacy systems, particularly in procurement and financial operations. For example, despite strong interest in automation, 39% of procurement teams report that most processes remain manual, 38% cite poor integration between specialized tools, and 34% describe their tech stacks as too rigid to modify (Digital Commerce 360, 2025). Data silos and limited IT bandwidth further slow deployment. These constraints help explain why B2B adoption, while economically compelling, may progress incrementally, with pilots outpacing full production rollouts.

New monetization models needed for agentic systems

As agentic commerce scales, agents increasingly need to be paid for the work they perform, requiring fundamentally new payment flows and business models. Futurists predict a world with billions of specialized agents, and early signals are already visible: thousands of independent builders are creating agents using platforms like n8n, Dust, and Buildship, echoing the rapid rise of “vibe-coding” tools, where over 25 million applications have already been built on Lovable. This explosion of agents exposes two structural breaks with traditional software economics.

SaaS pricing no longer works

Traditional software follows deterministic workflows, the same input produces the same output at predictable costs. AI agents operate probabilistically: they may retry failed operations, explore multiple solution paths, or require varying amounts of compute to reach the same goal. A simple task might cost pennies one day and dollars the next, depending on how many attempts the agent needs. This fundamental unpredictability breaks flat subscription models. Agent businesses must shift toward usage-based, outcome-based, or workflow-based pricing that reflects actual consumption. Yet there is no standardized infrastructure to meter agent activity, bill at fine granularity, and settle payments in real time. Startups such as Paid.ai, Alguna, Nevermined, are emerging to fill this gap, building the metering, billing, and settlement layer required for agent-native monetization.

Agent-to-agent transactions need new payment rails

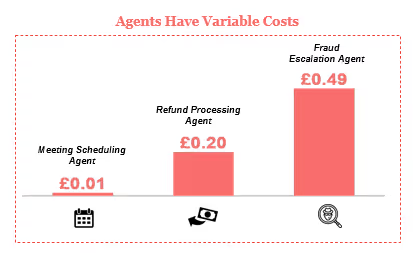

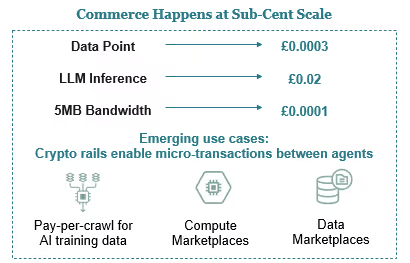

Complex multi–agent systems call on specialised agents to perform sub-tasks. As agents transact for data, inference, and bandwidth, the value exchanged is measured in fractions of a cent, far below what card networks and bank rails were designed to handle. Fixed fees, chargebacks, and batch billing overwhelm these transactions and make real-time, granular settlement uneconomic. Consider a future workflow: A user uploads a podcast to ChatGPT and asks it to transcribe and analyze the content. ChatGPT lacks native transcription capabilities for this specialized format, so it calls an external voice-to-text agent built by an independent developer. A metering platform like Paid.ai tracks the usage and settles a payment of £0.003 to the developer agent via crypto rails. The transcript is returned to ChatGPT within seconds, which then delivers the analysis to the user. Traditional payment infrastructure makes this impossible: a £0.20 card processing fee on a £0.003 transaction represents 6,600% overhead. The agent-to-agent service call simply cannot happen at scale economically. Crypto-native rails resolve this mismatch by enabling near-zero-cost, programmable micro-payments, unlocking pay-per-use pricing and autonomous agent-to-agent markets. This infrastructure underpins an emerging agent economy, led by builders such as Crossmint, Olas, and Payman.

The Infrastructure Gap

The promise of agentic commerce is vast. Yet, with 95% of projects failing to reach production, the path to scale depends on solving the identity, data, and payment gaps that keep agents stuck in pilot mode.

Despite hundreds of startups selling the “picks and shovels” of agentic commerce, real-world adoption remains extremely low. As of August 2025 95% of AI agent projects are failing, highlighting a widening gap between experimentation and durable deployment (MIT, 2025). The bottlenecks are readiness and infrastructure.

The first constraint is a readiness gap. Consumers do not yet trust agents to act autonomously on their behalf, regulators are imposing requirements before compliance infrastructure exists, and merchants are actively resisting intermediaries that threaten their business models. Enterprises are deploying agents faster than their foundations can support: decades-old systems built for human workflows are being stretched to accommodate autonomous execution, creating fragility beneath otherwise compelling use cases.

The second constraint is an infrastructure gap. The core building blocks that agents need to operate safely and at scale, identity, permissions, payments, and integration standards, are still immature. As a result, startups are forced to assemble fragmented, non-standard solutions, keeping most agent deployments stuck in pilot mode.

The Infrastructure Gap

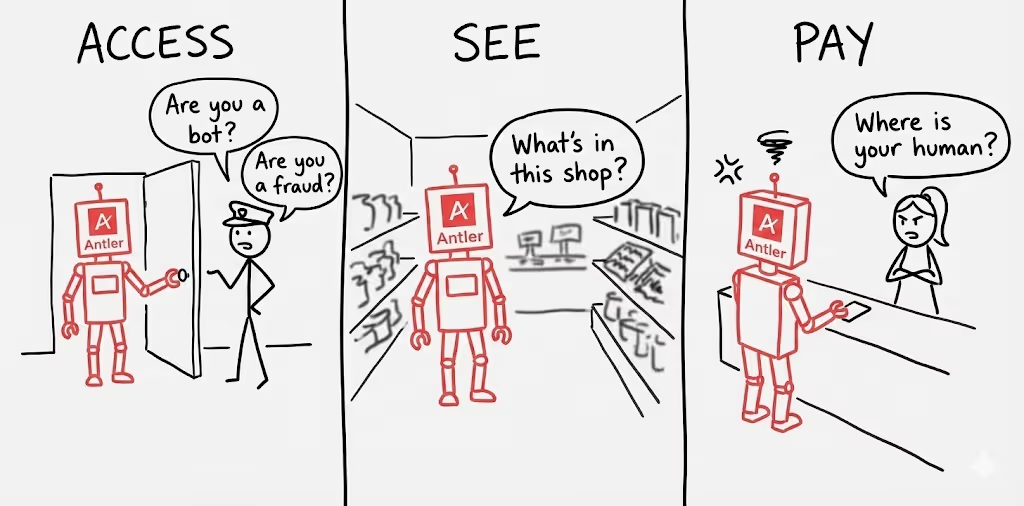

As investors in technology, we’re particularly interested in what infrastructure needs to be solved to enable this new dawn of agentic commerce. Using the analogy of in-store shopping, three missing capabilities separate experimental agents from production-grade systems: agents must be able to access the store, see what’s in the store, and pay in the store.

The market map below shows where innovation is emerging across the infrastructure that enables agentic commerce.

.avif)

“Access the Store”: For an agent to initiate a purchase, a merchant must be able to answer two basic questions: who is this agent and what is it allowed to do. Today, neither can be answered reliably.

- Agent identity, or “Know Your Agent” (KYA): There is no standardized way to attach a cryptographically verifiable identity to an agent acting within a purchase flow. As a result, merchants cannot distinguish a legitimate shopping agent from a headless browser, a bot scraping prices, or a bot executing fraud. Companies working on this include Anon, Neural Payments*, Skyfire.

- Delegated spending authority: Even if an agent’s identity were known, there is no machine-readable framework to define the scope of its permissions. Agents need explicit, enforceable constraints, such as spend limits, merchant limits, category restrictions, or approved SKUs, that can be verified automatically at the point of transaction.

- Fraud and authentication mechanisms: Existing solutions assume a human decision-maker and rely on challenges like 3DS, one-time passwords, or biometrics, which autonomous agents cannot complete. As a result, pilots succeed only by bypassing these controls, while production deployments remain unsafe or infeasible. Companies building across this space include auth0, Stytch .

- Standardized protocols for agent access: Machine verifiable assurance of an agent’s identity, permissions, and payment authority; early examples include Google’s Agent Payments Protocol (AP2), Visa’s Trusted Agent Protocol (TAP), Skyfire’s KYA (Know Your Agent) identity verification for agents, Catena Labs’ ACK-ID, and Nevermined ID.

“See the Store”: Even when an agent is trusted and authorized, it struggles to act because product data and workflows are not exposed in a form agents can reliably interpret or execute against.

- Storefront & merchant data: Product details like price, availability, variants, and fulfillment terms are embedded in unstructured pages, forcing agents to infer intent rather than reason deterministically. Without normalized, machine-readable storefront data, agents cannot reliably compare inventory or make consistent decisions. Companies working on this include New Generation, Merchkit*, Swap, Colossal, Catalog, Commerce Clarity.

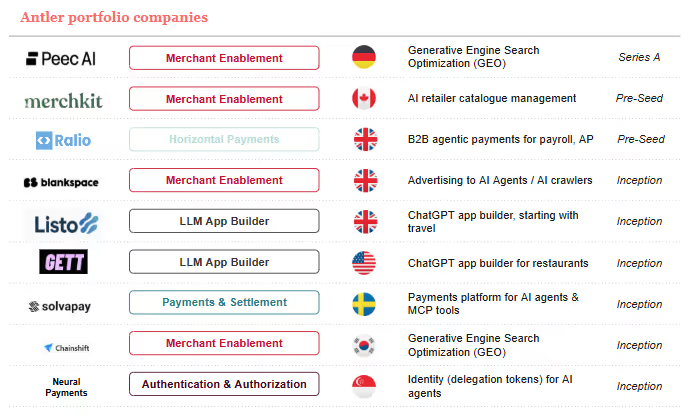

- GEO / Agent EO: Even when product data exists, agents struggle to discover it. Merchants need to optimize content for agent consumption, structuring product information, brand positioning, and inventory details so agents can find, understand, and recommend their offerings. Without agent-optimized content, merchants risk invisibility in a world where discovery happens through ChatGPT and Perplexity instead of Google search. Companies working on this include Bluefish, Chainshift*, Peec*, Profound, Wilgot.

- Data Monetization & Content Licensing: The economic model breaks when agents consume merchant content without generating traditional ad revenue or engagement metrics. Merchants need infrastructure to monetize agent access, metering how many times agents query their catalogs, licensing product data for agent training, and capturing value when agents browse without humans clicking. Without clear compensation mechanisms, merchants may block agent access entirely. Companies working on this include Blankspace*, Skyfire, Tollbit.

- Browser automation & web navigation: When clean APIs don’t exist, agents still need reliable ways to operate legacy e-commerce interfaces built for humans, logging in, selecting products, and progressing through multi-step flows. The gap is dependable browser-level execution that can handle real-world UX variation without breaking. Companies working on this include Bright Data, Browserbase, Browser Use, Exa, Parallel, Skyvern.

- Tool discovery & API orchestration: Commerce workflows span multiple systems, from inventory and pricing to shipping and payments. Agents need ways to discover the right tools and reliably chain them into end-to-end workflows. Without orchestration, execution remains brittle and incomplete. Companies working in this space include Anon, Composio, Wildcard.

- LLM App Builder: Merchants and developers need platforms to build and deploy commerce agents without rebuilding infrastructure from scratch. These end-to-end platforms provide agent creation interfaces, payment integration, distribution to channels like ChatGPT or Perplexity, enabling merchants to launch agent-native experiences quickly. Without builder platforms, only large retailers with engineering resources can participate in agent commerce. Companies working in this space include Gett*, Latinum, Listo*, Vypr, Alpic.

“Pay in the Store”: Current payment infrastructure was designed around human authentication and static credentials, leaving agents without the primitives needed to transact autonomously.

- Tokenization & security: Agents need cryptographically secure tokens that allow them to transact without exposing raw payment data, while enforcing constraints on spend, category, merchant, and timeframe. Today’s virtual cards serve as a stopgap, but they lack fine-grained control, revocability, and machine-verifiable scope, making them unsuitable for large-scale autonomous use. Companies working in this space include Locus, Mesta, Nekuda, Neural Payments*, Token Flow.

- API enabled checkout: At the point of payment, agents need programmatic access to calculate final transaction terms, tax, shipping, duties, discounts, and total price, and execute payment once confirmed. Today, these calculations are embedded in human-facing checkout flows, preventing agents from reliably validating pricing, ensuring compliance, or reconciling authorization with settlement. Companies building in this space include Firmly, Henry Labs, Rokt, Rye.

- Agent metering and billing: Agent-driven commerce produces granular, variable activity that cannot be captured by subscriptions or monthly invoices. Without infrastructure to track usage, price actions accurately, and settle payments in real time, autonomous agents cannot be governed or monetized reliably. Companies building in this space include Alguna, Nevermined, Olas, Paid, Solvapay*.

- Companies building payment flows across all three infrastructure layers include Sapiom, Catena, Crossmint, Natural, Payman, PayOS, Skyfire, Ralio*.

*Antler companies

Key Lessons Learned for Investors and Builders

- Consumer adoption will outpace B2B: B2B use cases for agentic commerce are compelling, but adoption may be slower than expected due to legacy constraints. Many enterprises are deploying agents on top of systems never designed for autonomous execution; for example in procurement, 34% operators claim their tech stacks are too manual to modify (Digital Commerce 360, 2025). As a result, B2B adoption is likely to be incremental, advancing workflow by workflow rather than scaling quickly. Consumer adoption may move faster once trust barriers are crossed. While only 10% of consumers have used AI for purchases, 64% say they are open to doing so, indicating significant latent demand (Bain, 2025). Crucially, consumer agent interactions are concentrated within trusted LLM platforms like ChatGPT, Perplexity, and Gemini. If transaction flows become native to these interfaces, adoption could follow a J-curve, with rapid acceleration once the experience feels seamless.

- Timing risk is real, start-ups are building on shifting sands: The core infrastructure required for agentic commerce is still immature and fragmented. Critical layers, including protocols (ACP, X402, MCP), authentication and security (KYA, tokens), access (APIs and browser infrastructure), and payment rails, are evolving in parallel, increasing execution risk. As a result, many startups are betting that the market materializes before their runway expires. Gartner predicts that 40% of AI projects will fail by 2027, largely because current models and systems lack the maturity and agency required for complex business goals (Gartner, 2025). Startups who first serve existing payment flows (retail, procurement, payroll) will monetize faster and are more likely to survive to see true agentic innovation. Still, the size of the prize for building the core infrastructure that powers the future of commerce is enormous.

- The winners will be connective tissue, not new rails: Historical infrastructure winners have succeeded by abstracting away complexity rather than rebuilding foundational systems. Plaid unified tens of thousands of bank integrations behind a single API; Stripe reduced months of payment compliance work to a few lines of code. The same dynamic is playing out in agentic commerce. Today’s opportunity lies in simplifying what already exists, through agent-native authorization and access (KYA) that allows agents to safely interact with existing systems, storefront and data aggregation that normalizes merchant catalogs for agent adoption, and horizontal payment orchestration that routes transactions across Visa, Mastercard, PayPal, crypto, and emerging rails. Value accrues to those who make legacy systems usable by agents, not those who attempt to replace them.

If you’re building in the space and are looking to next raise your Series A or Series B, reach out to elevate@antler.co.

Or if you’re just getting started, Antler runs residencies across 27 cities globally. You can apply to the relevant location here.

ANTLER RESIDENCY —LAUNCH YOUR STARTUP

Antler backs exceptional founders to go further, faster.

.png)

.png)