.webp)

.png)

This article was co-authored by Keerat Sethi and Akshat Arya.

Neither of us are deeptech investors. We are generalists, and we came to robotics the way most generalists do: skeptically, and a bit late. Our backgrounds are in fintech, software, and consumer businesses. When robotics companies started showing up in our pipeline more regularly, our default reaction was somewhere between cautious interest and quiet scepticism.

That wariness was not unfounded. The graveyard of well-funded robotics startups is long. Anki raised over $200M and shut down. Attabotics raised CAD $200M and closed. AWS RoboMaker failed to gain traction. DoorDash acquired Chowbotics and then killed it. These were not underfunded or poorly managed companies. They ran into structural problems: unit economics that did not work, deployments that could not scale, and software that was not good enough to deliver consistent commercial value.

And then, over the last 18-24 months, something in the evidence started to shift. Not just in the pitch decks, which have always been compelling, but in what was coming out of early deployments: the cost curves on components, the quality of foundation models being applied to robot policies, and business model structures that were finally making customer ROI more legible.

This piece is our attempt to lay out our (still) early thinking around this space, where we find real investment opportunities exist, and what we are doing about it.

PART 01

The Inflection Point: Why Now Is Different

Every technology wave reshapes robotics

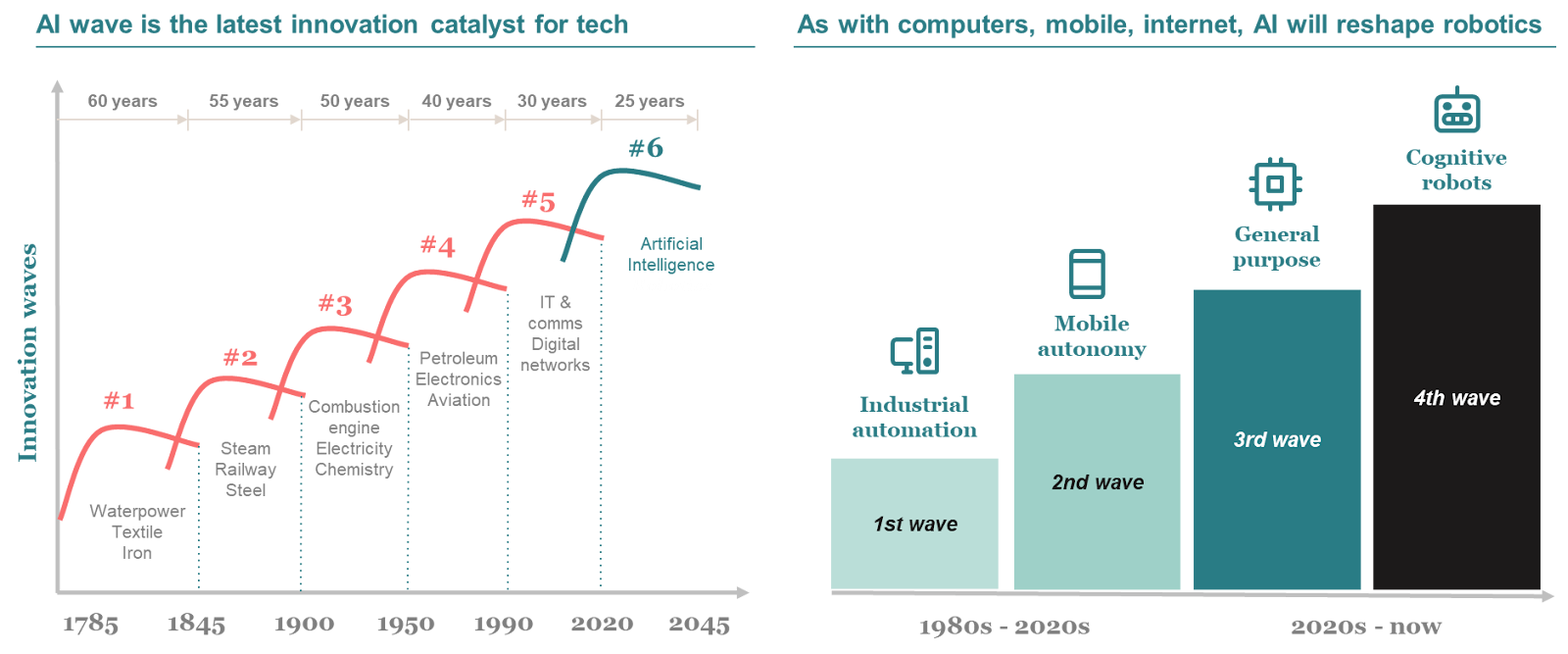

When you plot out the major innovation waves since the Industrial Revolution, there is a pattern. Each wave reshapes the industries and capabilities of the one before it. Water and steam power gave way to electricity. Electricity gave way to electronics. Electronics gave way to digital networks. And now the latest AI wave is beginning to reshape what came before it.

Robotics went through several distinct phases inside this broader arc. Industrial automation from the 1980s onward gave us the assembly-line robots you see in factories. Mobile autonomy through the 2000s and 2010s brought warehouse robots and early autonomous vehicles. We are now crossing into cognitive robotics, where AI provides the intelligence layer that makes robots genuinely adaptive to the real world rather than just executing pre-programmed scripts.

The critical shift is this: in every prior wave, hardware led and software tried to keep up. Robots could move, but not think. Today, however, the software and model infrastructure is catching up.

What the last decade taught us

Before getting to why things are different now, it is worth being direct about why the prior decade failed commercially. Three things broke most robotics companies.

First, unit economics were structurally broken. Hardware costs of $100K to $500K per robot upfront, combined with 50 to 70 percent initial utilization rates, meant customers were sitting on expensive assets that were idle for nearly half the time. ROI was theoretically positive on paper and genuinely hard to achieve in practice.

Second, every deployment was essentially a custom integration project. Every site required bespoke safety configurations, manual tuning, and heavy professional services. That made it nearly impossible to scale, because the 10th customer was almost as expensive to onboard as the first.

Third, and the most important one, the software layer simply was not good enough. Robots could execute scripted tasks in controlled environments. They could not handle variance, recover gracefully from edge cases, or generalize from one setting to another. The intelligence was too brittle.

The companies that raised hundreds of millions and failed mostly failed on one or more of these three dimensions. It was not a technology problem in the narrow sense. It was a systems problem: the whole stack needed to improve simultaneously. And that is now happening.

Reasons why we believe the tipping point is real

1. Demand pull has fundamentally changed

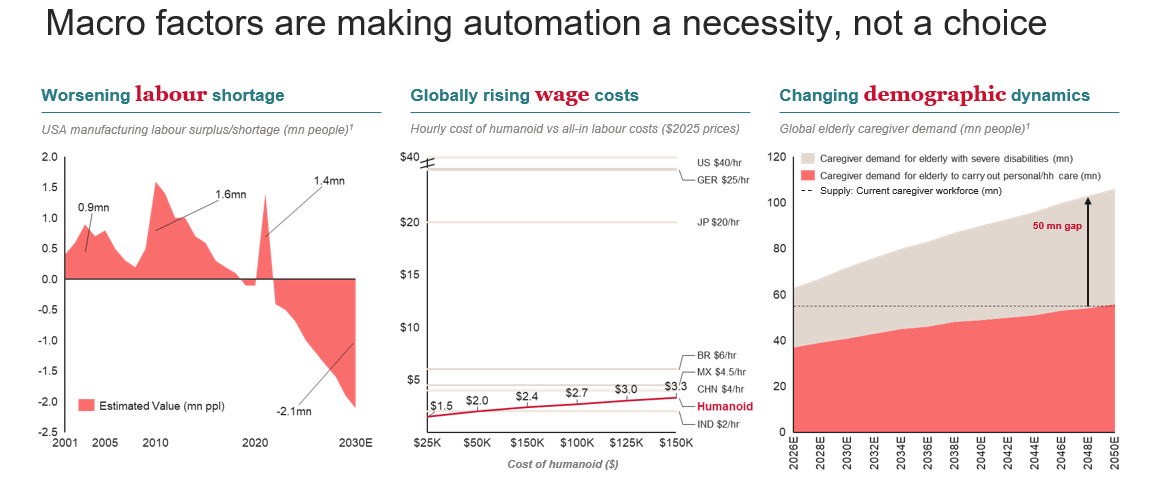

Automation has moved from a productivity enhancement to a workforce necessity in certain sectors. US manufacturing is projected to face a labor shortfall of 2.1 million people by 2030.

At the same time, when a humanoid robot costs anywhere around $25K to $100K to manufacture and the all-in hourly cost of a US warehouse worker is $40/hr, the economics of substitution become increasingly compelling at scale (Goldman Sachs Research).

Demographic dynamics are making this more acute beyond manufacturing. Globally, caregiver demand for the elderly is expected to outpace supply by 50 million people by 2050, with no realistic path to closing that gap through human labor alone. Robots are not just replacing workers in these contexts. They are filling roles that would otherwise simply go unfilled.

2. Foundation models have become the new baseline

Three years ago, building a robotic policy for a new task required months of manual data collection and training. Today, teams can start from pretrained vision-language-action models and fine-tune with substantially smaller datasets. Google DeepMind's robot transformer work, NVIDIA's Isaac GR00T N1 initiative, and open-source efforts like Hugging Face's LeRobot have collectively lowered the barrier to entry substantially.

The number of robotics-related research publications has grown from roughly 2,000 per year in 2016 to approaching 22,000 in 2024 and 2025 (Coatue Report) . Robotics is entering a compounding phase where shared papers, datasets, and model weights are accelerating iteration in the same way open-source software did for the software industry in the 2000s.

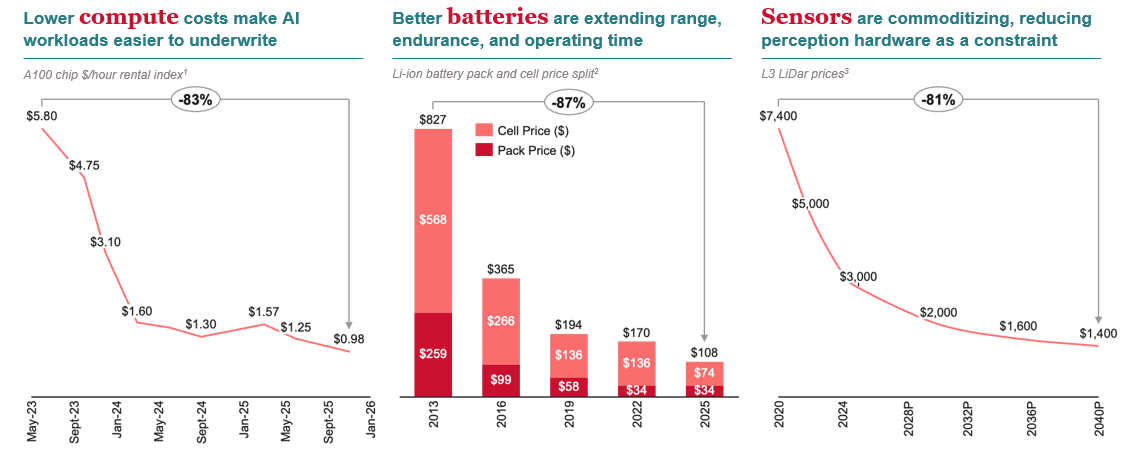

3. Component and compute costs have fallen dramatically

The cost curves across compute, batteries, and sensors are moving in the right direction simultaneously and rapidly. A100 chip rental costs have dropped 83% since mid-2023 (Silicon Data). Li-ion battery pack prices have fallen 87% since 2013 (BloombergNEF). L3 LiDAR prices have come down 81% from their peaks and are projected to continue declining through 2040 (Coatue Report). Each of these individually matters. Together, they are transforming the unit economics of deploying intelligent robots at scale.

4. Hardware and software performance has crossed a critical threshold

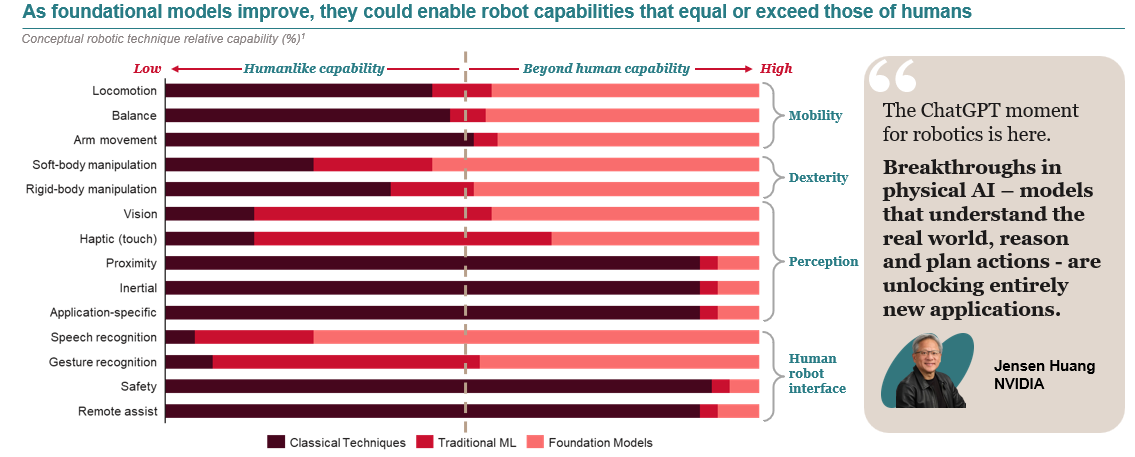

This one is harder to quantify, but it is real. Boston Dynamics' Atlas evolution provides a great illustration of the arc: in 2014, it was being trained to maintain balance in different terrains. By 2019, it was performing whole-body dynamic maneuvers. By 2023, it was combining locomotion and dexterity for multi-step manipulation tasks. By 2025, it had transitioned from a hydraulic research prototype to an electric industrial system being used in Hyundai's automotive manufacturing operations.

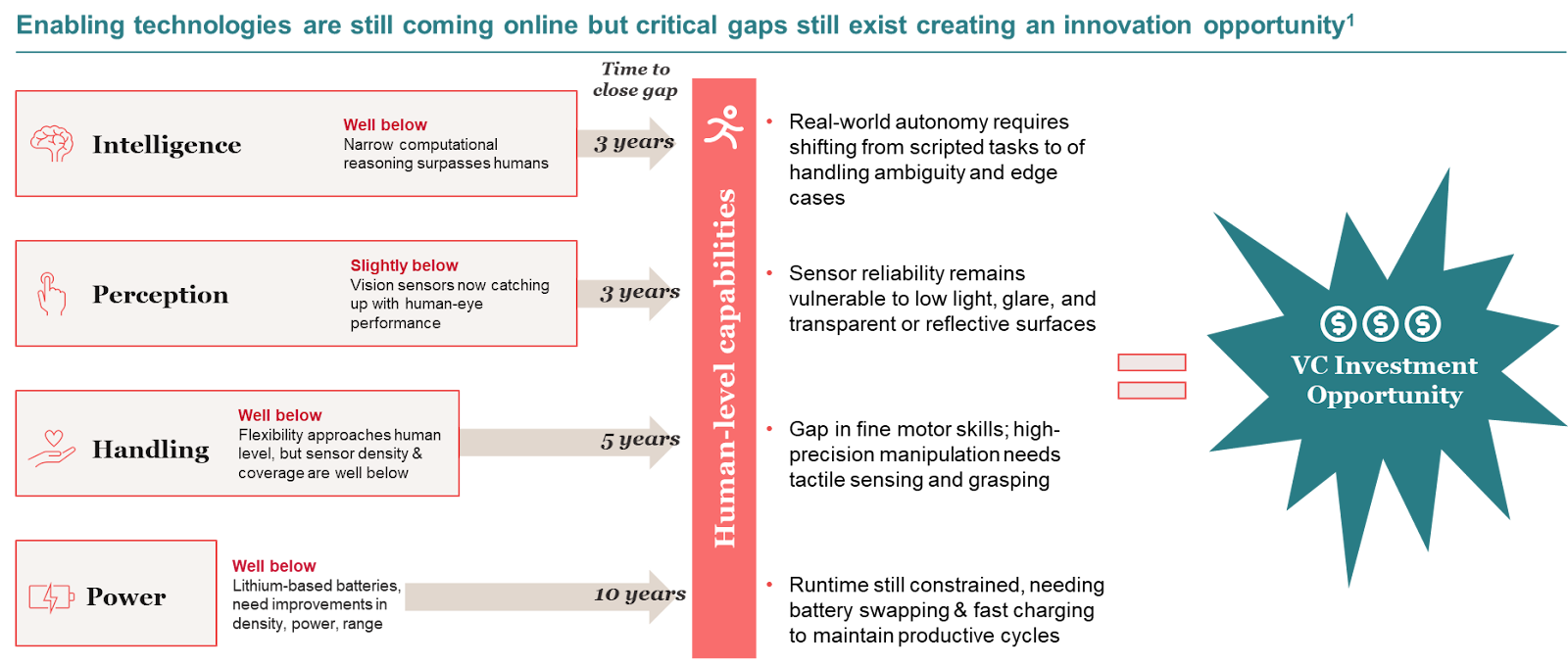

McKinsey data on conceptual robotic capabilities shows that foundation models are pushing mobility and perception toward or beyond human-level performance on key dimensions. Proximity sensing, inertial systems, and application-specific sensors are already well beyond human benchmarks. Locomotion and balance have reached human-equivalent ranges. The gaps that remain, particularly around fine motor dexterity and handling, are real but narrowing.

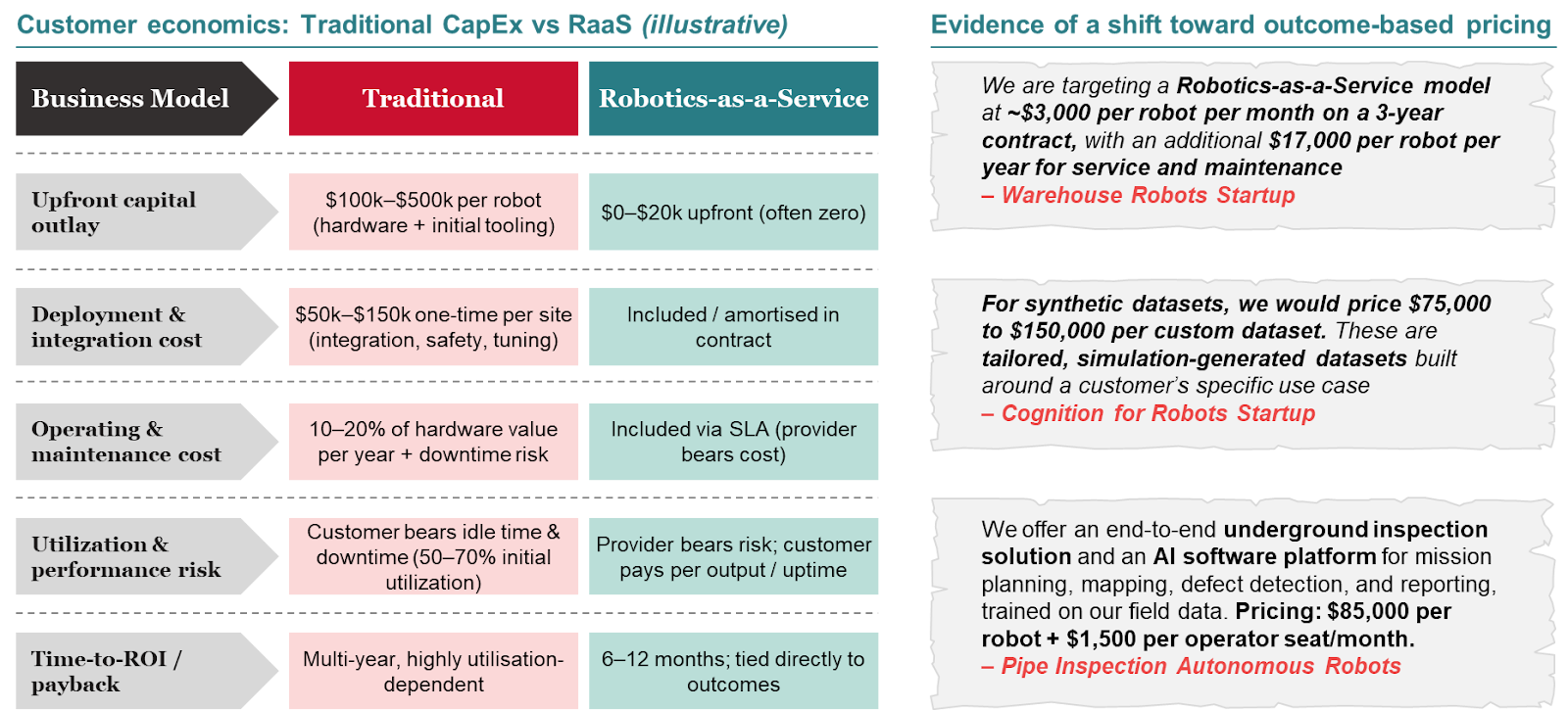

5. Business models now align with customer ROI

A structural reason prior robotics deployments failed commercially was not just hardware unit economics. It was that customers had to bear all the risk. They paid $100K to $500K upfront, then paid again for integration, then paid ongoing maintenance fees, and still absorbed the downtime risk themselves.

Robotics-as-a-Service changes this completely. Customers pay zero to $20K upfront. Integration and maintenance are amortized into the contract. The provider bears the uptime risk. Time to ROI compresses from multi-year payback periods to 6 to 12 months tied directly to operational outcomes.

The pricing signals we are seeing from companies in our pipeline reinforce this. One warehouse robotics company we spoke with is targeting approximately $3,000 per robot per month on a three-year RaaS contract. That model converts what was a capital expenditure decision requiring board approval into an operational expenditure decision that a logistics VP can make.

6. The remaining gaps are real…but provide a window for new investment

That being said, we want to be careful not to oversell the maturity here. Physical AI progress is real, but the stack is not fully built.

Real-world autonomy still struggles with ambiguity and edge cases. Sensor reliability degrades in challenging light conditions. Fine motor manipulation requiring dense tactile feedback is still roughly 5 years away from human equivalence. Battery runtime is a decade-scale problem. Throughput and offtake of robots in real-world environments are still 20-50% (Bain Report) of human levels.

The gaps that remain are engineering problems with reasonable credible solution paths, not scientific unknowns. That distinction matters for how you think about investment timing.

PART 02

The PhysicalAI Playbook: Where the Opportunity Actually Sits

The industries being reshaped

Robotics will unlock $675B of disruptive economic value across industries, with manufacturing and mining ($84B), healthcare and social assistance ($81B), accommodation and food services ($71B), administrative support and government ($70B), and construction ($67B) leading the way (McKinsey Report).

The CEO-level signals are already visible. Jensen Huang has said humanoid robots will be widely adopted in factories within a few years (Reuters), not five as many expected. Andy Jassy has said Amazon expects to reduce its corporate workforce through automation over the next several years (CNBC). BMW's production line ran Figure's humanoid robot for 10 hours a day across 11 months, contributing to the manufacture of 30,000 cars (BMW).

Beyond replacement, robots are also expanding the addressable market. There are categories of work that humans genuinely cannot do: sustained nuclear facility inspection, continuous operation in chemical environments, disaster response in environments too dangerous for human entry. The TAM is not just about labor substitution. It is about enabling work that was previously impossible or uneconomical to do at all.

A framework for where to invest

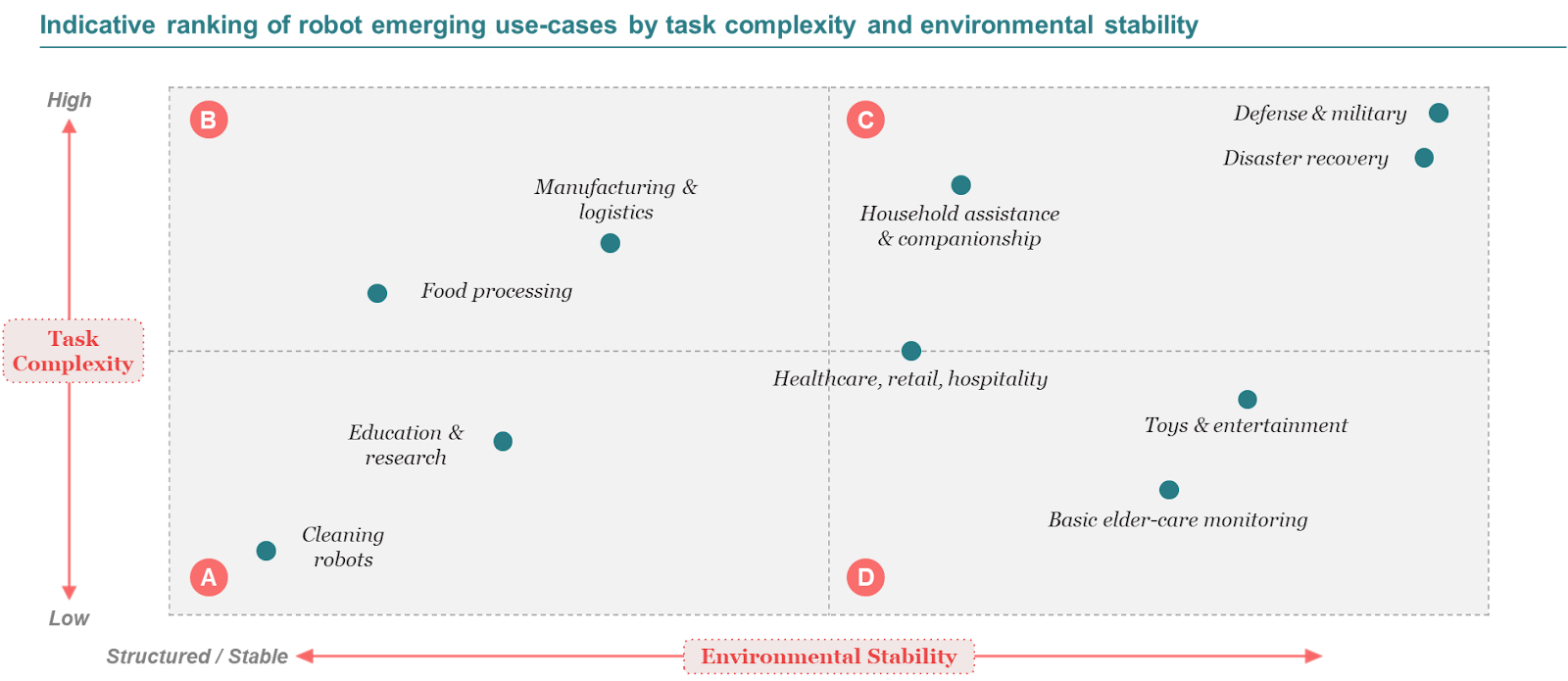

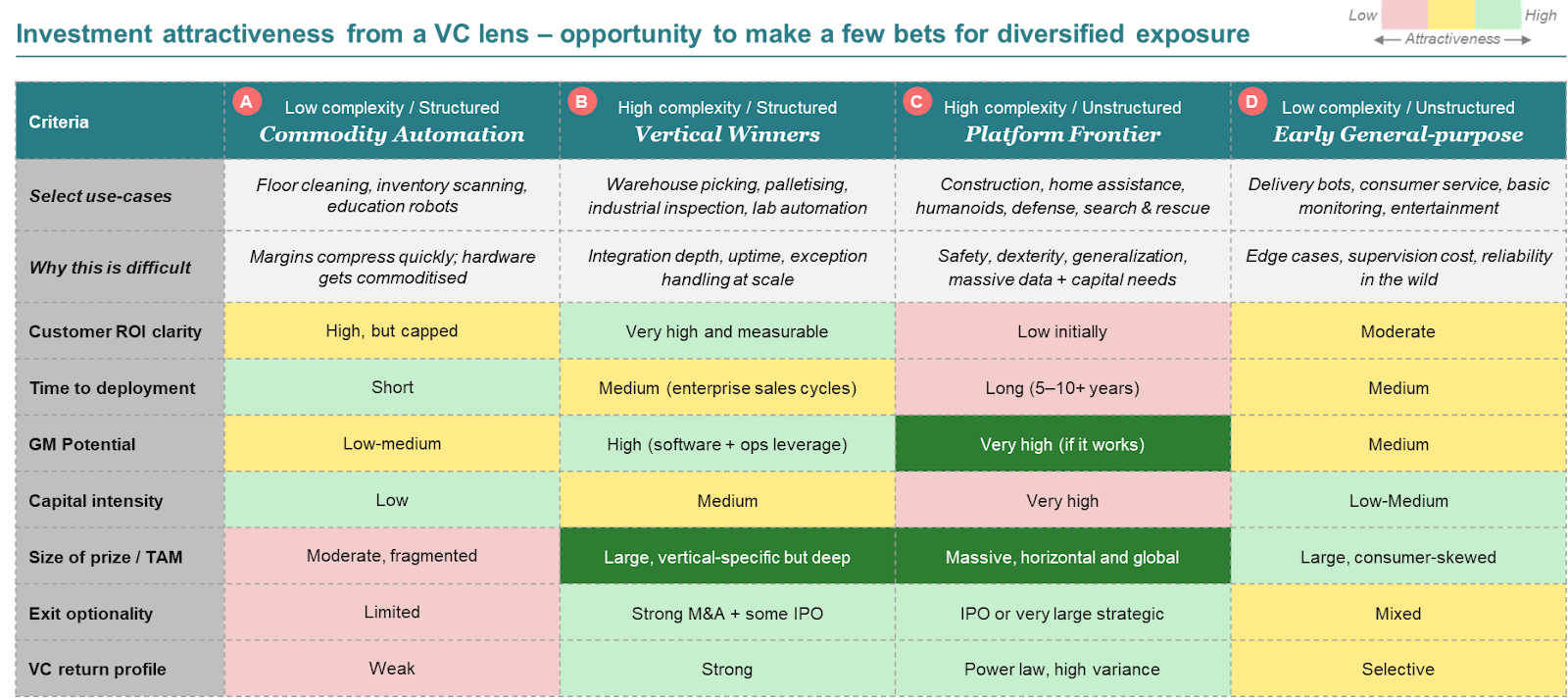

Not all robotics opportunities are created equal from a VC lens, and the way we think about it is through two dimensions: task complexity and environmental stability.

For low-complexity tasks in structured environments, you get commodity automation. Floor cleaning, inventory scanning, basic education robots. These are potentially steady, stable businesses, but from a returns perspective the profile is weak. Margins compress quickly, hardware gets commoditized .

In high-complexity structured environments, you get vertical winners. Warehouse picking, palletizing, industrial inspection, lab automation. This is where we can see strong VC returns over the next 5 to 7 years. Customer ROI is high and measurable. Gross margin potential is strong because software and operational leverage compound over time. Enterprise sales cycles are the key constraint, not technical feasibility. Exit optionality is strong through both M&A and IPO.

The upper-right quadrant, high complexity in unstructured environments, is where humanoids and general-purpose robots live. The potential is genuinely massive. But so is the capital requirement, and time to meaningful deployment is 5-plus years in most cases. The return profile is power law with high variance. A few will generate extraordinary outcomes.

The lower-right, low complexity in dynamic environments, covers delivery bots, consumer service robots, entertainment. We can see interesting niches here, with moderate TAMs . Worth watching opportunistically but not where we are concentrating.

The full picture is wider than the 2x2

The matrix is a useful orientation, but it only captures part of what we find interesting. When you map out the full robotics value chain, a meaningful slice of the opportunity sits not in the end applications themselves but in the enabling infrastructure that makes those applications possible: foundation models, training data pipelines, simulation environments, developer tooling, deployment infrastructure, and the software that helps teams understand what their robots are actually doing in the field.

Some of these companies are horizontal plays serving the whole ecosystem. Others are closely tied to specific workflows or robot types. Either way, they are a core part of the stack and, in our view, still under-focused relative to their strategic importance – with interesting companies like Drift (AI copilot for robot simulation), Alloy (robotics data search and analysis), Imitation Machines (imitation learning infra), and Lucky Robots (AI-powered virtual robot training) alongside more application-layer bets.

We have also become more interested in the build approach at the application layer. There is a meaningful difference between companies assembling a robot from third-party components and those taking a more integrated, full-stack approach (like Holiday Robotics). Full-stack is harder to execute, but when it works it creates tighter feedback loops between hardware, software, and real-world deployment data that compound over time. Antler’s global portfolio reflects this breadth: we have backed 20+ robotics and Physical AI companies at the early stage, across the stack, from developer tools and simulation through vertical applications in logistics, agritech, inspection, and industrial automation, to more horizontal platforms. The market map below captures where some early-stage companies are playing across the stack today.

.png)

What it takes to win

The car industry in the 2010s is a useful reference. Porsche, BMW, Audi, Toyota were all making excellent cars. Largely undifferentiated on a spec sheet. Then Tesla built a software and AI layer that made its cars genuinely different, and the market priced that difference at a significant premium.

For founders building in this space, the implication is clear: investing in hardware differentiation without a software moat is building on sand. The defensible position is the data flywheel, the proprietary training infrastructure, and the workflow integrations that make your system stickier than a competitor's. Winning requires scaling the system, not just building the robot

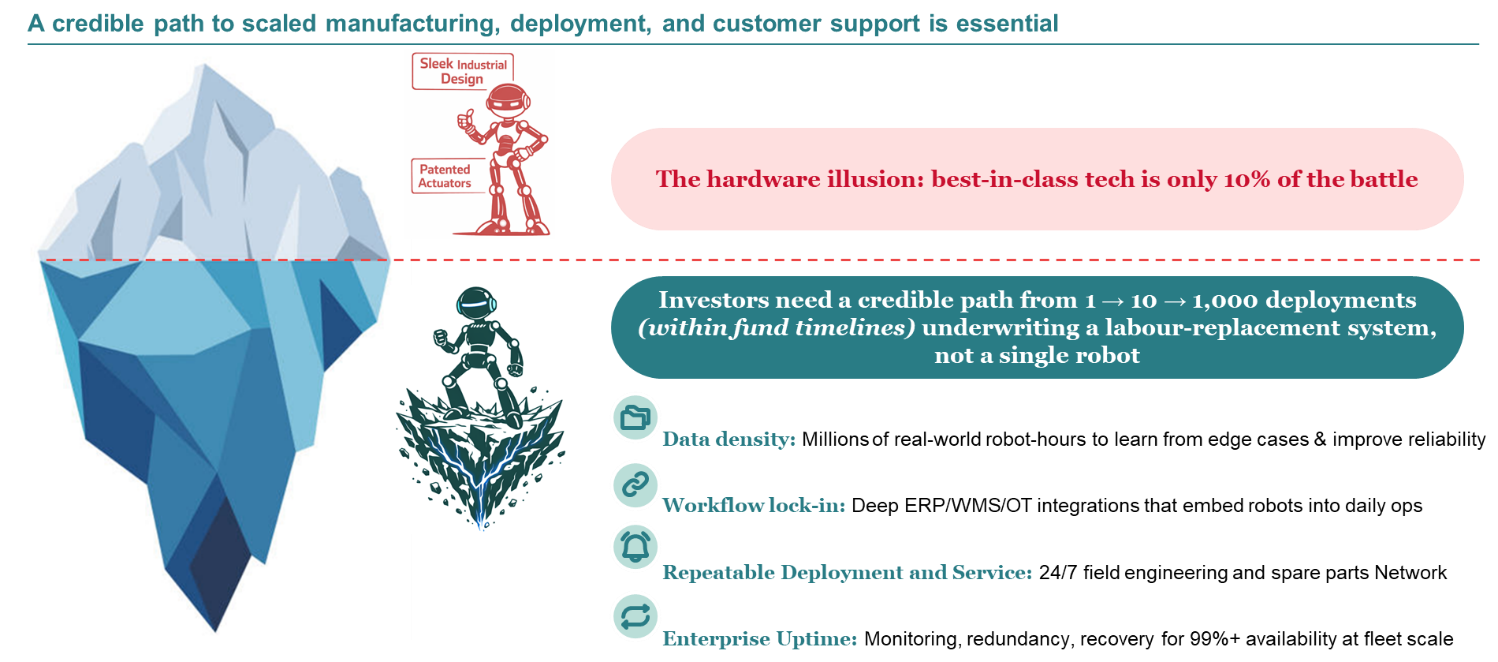

The common mistake we see when evaluating robotics companies is overweighting hardware quality as the primary criterion. Best-in-class actuators and sleek industrial design are maybe 10 percent of the battle. The 90 percent below the waterline is what actually determines whether a company succeeds commercially.

Specifically: does the company have a credible path to accumulating millions of real-world robot-hours to learn from edge cases and improve reliability over time? Does it have the ERP, WMS, and operational technology integrations that embed the robot into daily workflows, creating genuine switching costs? Does it have the 24/7 field engineering and spare parts infrastructure to deliver 99-plus percent uptime at fleet scale? And critically, does it have a repeatable deployment playbook that allows it to go from 1 to 10 to 1,000 sites without the economics deteriorating?

From an investment standpoint, we are underwriting a labor-replacement system, not a single robot. The path from a successful pilot to a scaled fleet is where most companies break and the ones that have a credible path to get this right are the ones worth backing.

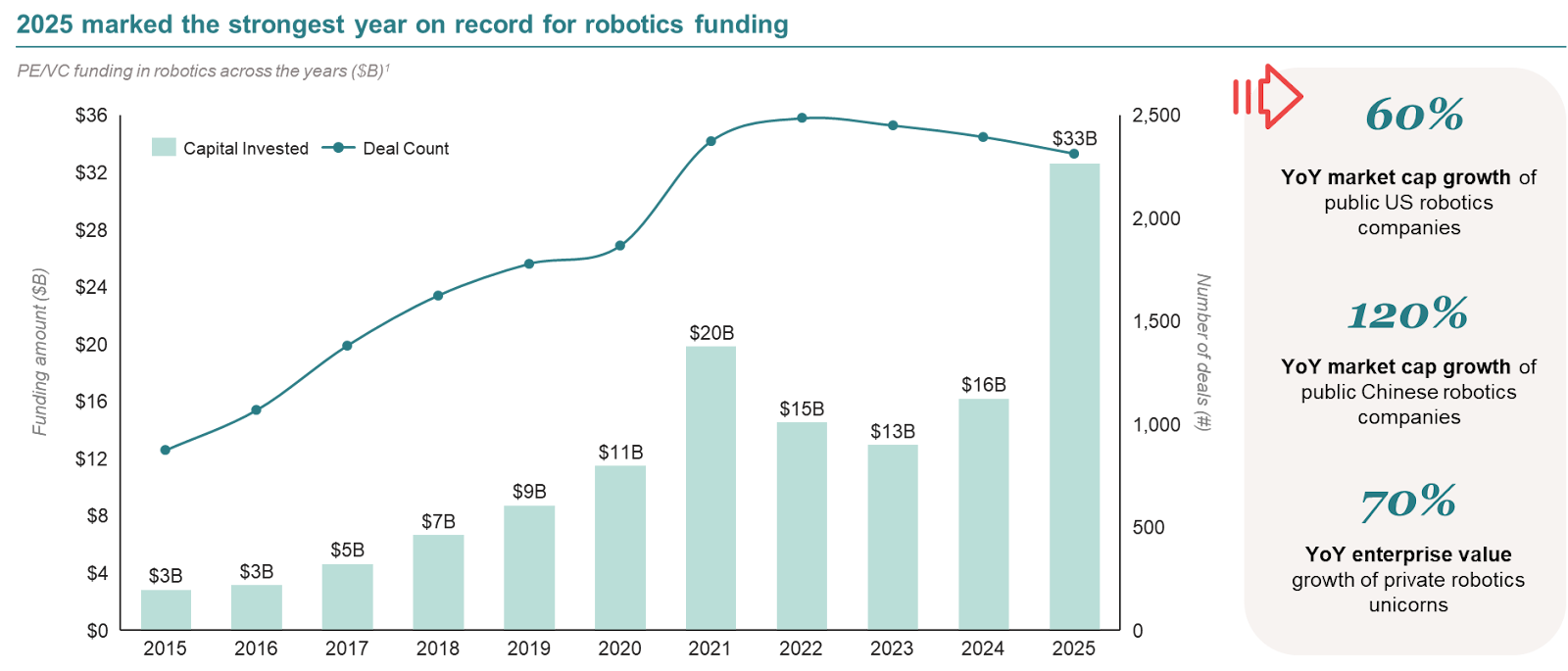

The funding picture

2025 was the strongest year on record for robotics funding, with PE/VC investment reaching $33B (Pitchbook). Public US robotics companies saw 60% YoY market cap growth. Public Chinese robotics companies saw 120% YoY market cap growth (F-Prime Report). Private robotics unicorns saw 70% enterprise value growth year over year.

Manufacturing, defence, and logistics are the segments attracting the most capital. Manufacturing robotics funding hit $25.7B in 2025, up from $9.7B in 2024. Defence robotics crossed $12B in 2025.

There is now over $203B (F-Prime Report) of private market value in robotics, with several companies achieving decacorn status. The defence segment alone accounts for $57B led by companies like Anduril, Shield AI, and Helsing. Autonomous vehicles collectively represent $55B with Waymo as the standout. General-purpose robotics is approaching $50B as a category with Figure, Physical Intelligence, and Apptronik leading the charge. Aggregate private market value in robotics grew 70 percent in 2025 alone.

Exit paths are materializing

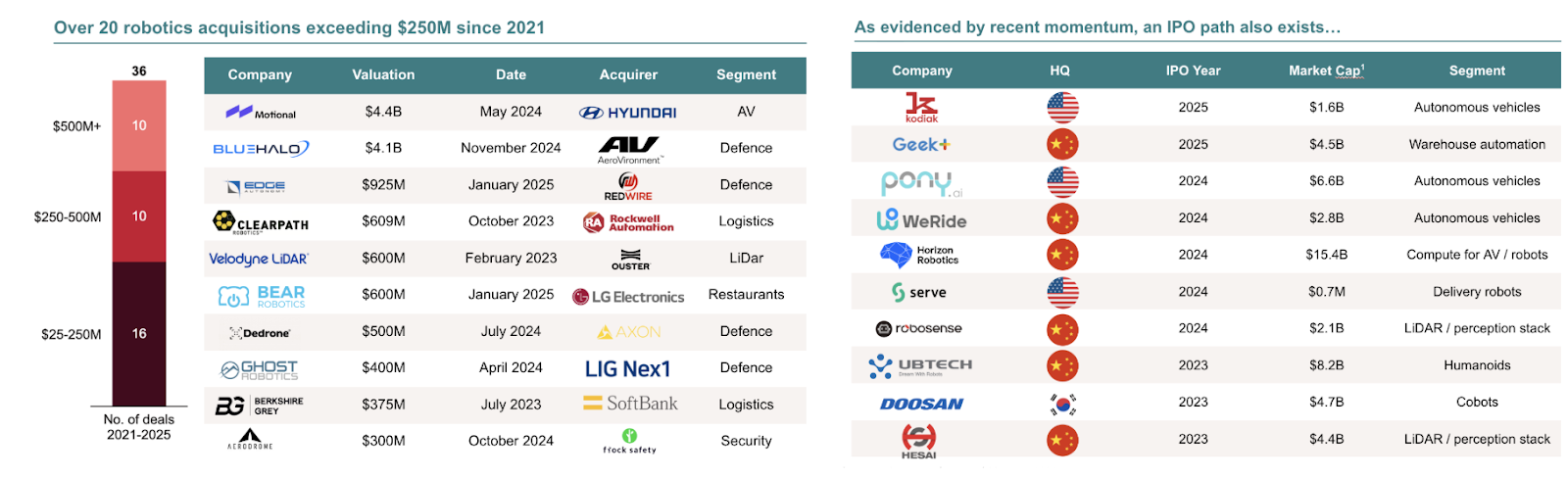

One of the things that held back robotics as a venture category was uncertainty around exit pathways. That uncertainty appears to be resolving.

On the M&A side, there have been 20+ robotics acquisitions exceeding $250M since 2021. The pattern is consistent: strategic acquirers are willing to pay premium prices because they can underwrite the operational value in ways that public markets discount.

On the IPO side, the last three years have produced a meaningful cohort of public comps, providing reference points for what the public market is willing to pay when robotics looks like recurring infrastructure rather than one-off hardware sales. The lesson from the IPO comps is: public markets reward predictability, operational leverage, and contracted revenue. Companies that can demonstrate improving gross margins, declining cost-to-serve, and high fleet utilization rates will have access to the IPO window.

Conclusions

We came into this exercise cautious, and are coming away genuinely excited. That does not mean everything being built right now will work. The hype is real, and there will be casualties. Companies that are primarily hardware plays without a software moat will face the same commoditization pressures that defined the last decade. Deployments that cannot scale without heavy custom integration will hit the same ceiling.

What has strengthened our view is not the narrative. It was the specifics. The cost curve data is real. The foundation model progress is measurable. Customer ROIs are finally something generalist investors can underwrite. And the structural labor shortage driving demand is not a cycle, it is a demographic. At the same time, critical gaps remain in intelligence, perception, dexterity, and reliability - leaving meaningful room for new companies to shape the next phase of the market. The combination of visible progress and still-open technical white space is what makes us so excited about the venture opportunity ahead.

If you’re building in the space and are looking to next raise your Series A or Series B, reach out to elevate@antler.co. Or if you’re just getting started, Antler runs residencies across 27 cities globally. You can apply to the relevant location here.

ANTLER RESIDENCY —LAUNCH YOUR STARTUP

Antler backs exceptional founders to go further, faster.

.png)

.jpg)