Key takeaways

This article outlines why early-stage access is critical and how investors can shape the next wave of outperformers by engaging early, globally, and across sectors—powered by AI, driven by impact, and aligned with real-economy transformation.

- Early-stage climate investing offers differentiated alpha, with investors shaping strategy, mission, and business model before value is widely recognized.

- Climate innovation is expanding beyond emissions into adaptation, food, water, and circular systems, with software-led models showing shorter time-to-scale and stronger M&A interest.

- AI is accelerating climate innovation by transforming physical challenges into scalable, data-rich solutions, especially in adaptation and resilience.

- Climate capital may begin to diversify beyond the US as investors respond to political uncertainty and seek regions with clearer industrial policy and stronger public-private alignment.

- The next generation of climate unicorns is likely to emerge in overlooked markets and underserved sectors, offering asymmetric upside for investors with early access and global reach.

_________________

A decade ago, climate action was framed as a moral imperative, a matter of sacrifice and an endless arc of responsibility. Today, it’s central to competitiveness and rebuilding the operating system of global commerce.

At first glance, the headlines might suggest a retreat from green ambition due to regulatory slowdowns in Brussels and political pushback in Washington, this is not a decline but a realignment. A recalibration of how economies compete, how capital moves, and how innovation scales. Climate innovation is moving from the periphery of philanthropy and policy to the center of economic strategy. And the smartest capital sees what’s next: climate innovation now underpins every sector, creating asymmetric opportunities for those shaping systemic change.

At Antler, we believe this is the moment for early-stage capital to lead.

From moral imperative to market logic

The narrative has evolved beyond merely "saving the planet" to transforming the systems we live by—energy, water, food, health, and infrastructure—to be more resilient, efficient, and profitable.

Recent analysis shows that climate tech funds have outperformed generalist VC by 9% IRR1 on average across recent vintages. AI is compressing costs, software is scaling impact, and macro shifts are creating new markets. Yet, venture allocations remain behind the curve. Climate tech makes up just ~10% of global VC investment, up from under 2% a decade ago, but still a fraction of the $6.3–6.7T needed annually by 20302.

This gap is early-stage VC’s edge.

Early-stage is where value and velocity converge

Early-stage investors help define product direction, pricing models, distribution paths, and even the mission itself. This is where strategic influence is highest and where the foundations for exponential growth are laid. The best backers spot exceptional individuals before the pitch is polished, before traction emerges, and before the market has caught up to the problem being solved.

Unlike public markets, which price outcomes already validated, early-stage investing captures value before the story is widely understood. That’s where the asymmetry lies, not in eliminating uncertainty, but in identifying where momentum is about to build.

Consider Tesla, Rivian, and LanzaTech. Each company went public with strong momentum, but the real value creation happened earlier. Enphase’s investors backed modular home energy when solar was still a niche market. LanzaTech pioneered carbon recycling before circular carbon markets existed. Tesla’s early-stage capital enabled it to survive its near-collapse and set the trajectory for the EV industry.

None were obvious. But all show what’s possible when conviction aligns with timing and talent. By the time these companies reached IPO, competition had intensified, valuations had risen, and much of the upside was already priced in.

The most compelling returns rarely go to those who wait. They are shaped at the point of origin when value is being built, not yet broadcast.

Climate unicorns: Concentrated today, expansive tomorrow

So far, climate unicorns have clustered in just a few geographies and sectors, mainly mobility and energy in the US and Europe.

Innovation is now moving into materials, food systems, water, and the built environment—sectors that are both underfunded and underserved. And the geography is shifting too. Emerging markets aren’t following the same path as the Global North, they’re leapfrogging it.

In markets where legacy infrastructure is limited or broken, new solutions don’t need to compete with incumbents. They can scale faster, at lower cost, and often with stronger unit economics. Consider:

- Africa’s electrification gap (600M+ lack electricity) is being addressed by decentralized solar microgrids integrated with mobile money, enabling pay-as-you-go models with customer acquisition costs up to 30% lower than Western platforms.

- Southeast Asia’s 250 million motorcycles are driving a lightweight EV boom. With vehicle costs of $1,500 to $3,000, swappable-battery e-motos are projected to create a $100B market by 2030.

- Vietnam’s rooftop solar capacity has grown 25-fold since 2017, powered by peer-to-peer trading apps and local developer networks, without reliance on state utilities.

- Agtech across the global south is tapping into a base of over 500 million smartphones, delivering AI-powered precision farming models with acquisition costs an order of magnitude lower than those in the West and representing a $250B import substitution opportunity.

Sources: IEA Africa Energy Outlook (2022). Provides Africa’s electrification needs and market potential, estimating over $90B+ in infrastructure demand. Asian Development Bank (2023). Light Electric Vehicles in Asia: Market and Policy Outlook. Projects $100B lightweight EV market by 2030 in Southeast Asia. BloombergNEF (2023). Vietnam Rooftop Solar Update. Reports 25x capacity increase in rooftop solar between 2017–2023, supported by peer-to-peer trading models. GSMA AgriTech & Carbonequity (2024). Mobile-enabled Agtech models across Asia reduce CAC up to 10x vs Western equivalents; linked to broader agri-import substitution opportunity ($250B+).

These aren’t fringe cases but early signals of where the next generation of climate unicorns is likely to emerge, outside the typical hubs, solving problems with localized, scalable, tech-driven models.

At the same time, political uncertainty in the US, particularly concerning the future of climate policy and industrial support, is prompting some investors to reassess geographic concentration. As questions grow about the durability of subsidies and regulatory tailwinds, we may see climate capital begin to diversify beyond a US-heavy approach. Regions like the Middle East, Europe, and Asia could benefit from this shift, offering more consistent industrial policy, rising tech ecosystems, and stronger public-private alignment in climate ambition.

For early-stage investors, this is geographic arbitrage in action. The playing field is broader, the paths to scale more direct, and the opportunities increasingly global. Those with the networks and conviction to invest beyond the obvious are best positioned to capture what comes next.

Climate is no longer a vertical, it’s a system-wide transformation

As climate innovation spreads across geographies, it’s also shifting across sectors and increasingly into areas that look and behave more like traditional VC opportunities.

Climate investing has long been synonymous with decarbonization. And while decarbonization still matters, the next wave of alpha lies in a broader transformation across food systems, water, health, circularity, and climate resilience.

This shift is evident in our portfolio, where over 60% of our climate-related companies tackle challenges beyond emissions. These companies are solving real-world problems with clear revenue pathways, shorter time-to-market, and growing M&A interest. They resemble the kinds of software-led and data-led models that have historically driven VC returns.

Adaptation and resilience, in particular, are emerging as high-leverage categories. Today, 71% of adaptation-focused VC funding goes into software and data3. Yet private capital in this space remains limited, presenting prime opportunities for first movers.

Deals grouped by climate outcome

.avif)

This is climate alpha in its next form: not just carbon-focused, but systemic, diversified, and deeply embedded in the real economy.

AI and climate: A compound advantage

AI is not diverting attention from climate but converging with it. Climate startups today are increasingly AI-native, leveraging machine learning, geospatial data, and IoT to solve physical problems with digital speed and scale.

From robotic agriculture to carbon accounting, these companies operate more like software ventures: lean teams, low capex, rapid feedback loops. That efficiency translates to performance—software-led climate startups now report 30% higher profit margins on average4, but it’s not just about software performance. These models turn previously opaque systems (forests, oceans, supply chains) into data-rich, investable domains.

This convergence is especially powerful in adaptation. As mentioned earlier, 71% of adaptation-focused VC goes into software and data. AI is the engine behind much of that shift. Smart grid analytics, biodiversity tracking, soil monitoring, PFAS detection, wildfire risk prediction, the list is growing, and the use cases are only becoming more precise and scalable.

More than half of Antler’s climate-related tech portfolio now incorporates AI, spanning the full stack from application-layer tools to deep-tech infrastructure and cross-sector enablers. These are the kinds of models that will define the next generation of high-performing, climate-aligned companies.

Yes, AI increases energy demand. Data centers could account for up to 12% of U.S. electricity consumption by 20305. But the sector is already iterating. AI-driven optimization, such as Nvidia's efforts to improve data center cooling efficiency, and new chip architectures are significantly reducing energy use. For example, Google has deployed its latest generation of Tensor Processing Units (TPUs) that are up to 2.7x more energy efficient than previous models, which has reduced their overall energy consumption in data centers. Breakthroughs like DeepSeek’s 95% more efficient training architecture8, suggests we may be underestimating AI’s potential to self-correct through innovation. The most forward-thinking founders are building solutions on both sides of the equation.

While Big Tech drives efficiency at scale, a new wave of early-stage startups is rethinking the architecture altogether. Startups like Vana and Flower are experimenting with decentralized training models. Their recent collaboration, COLLECTIVE-1, is a large language model trained across distributed GPUs using both public and user-contributed private data, without relying on centralized data centers. This approach reduces reliance on high-energy infrastructure and opens access to builders who cannot compete on scale alone. For climate-aligned innovation, this decentralized model could offer a more efficient, accessible path to AI development, one that aligns with both energy resilience and data sovereignty.

Early-stage is where these AI-native models are born, not retrofitted.

Our latest report features case studies of these AI-native, climate-aligned companies in action.

A market maturing for the better

2024 marked a clear inflection point for climate venture capital. The number of active investors declined as capital consolidated, reflecting a broader drop in sector-wide VC funding since 2022.

Annual investor count by stage 2020-2024 (no. of investors)

.avif)

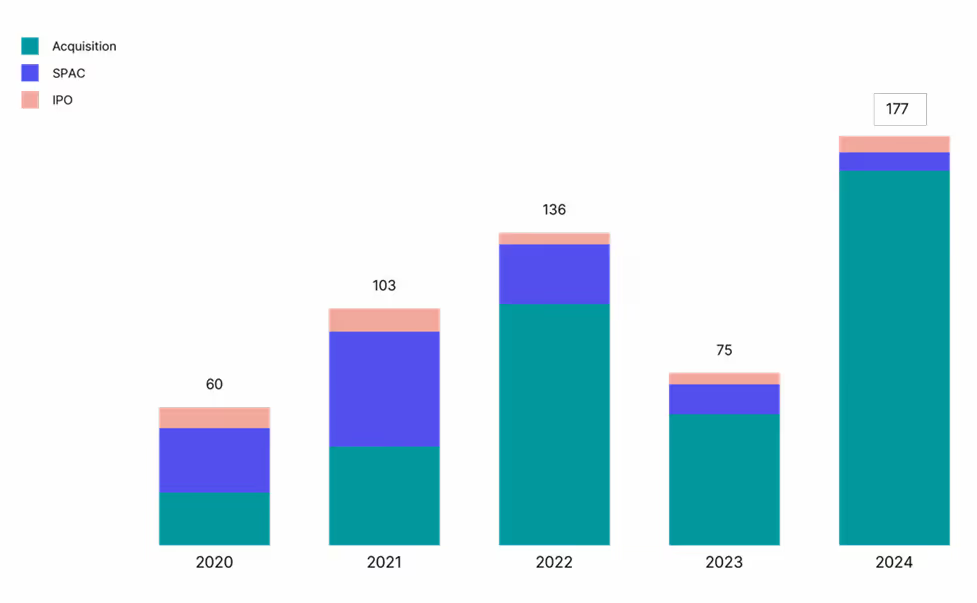

Yet, despite fewer new entrants, exits have accelerated—doubling in number—with acquisitions accounting for 92% of these exits7.

Climate exits (no.of exits)

Corporate buyers, not SPACs, are now driving climate exit momentum, particularly in AI-enabled solutions like autonomous agriculture and grid optimization. These startups are commanding premium valuations, often 20 to 200% higher than peers7, as seen in the March 2025 acquisition of Pearl Street Technologies by Enverus. A Carnegie Mellon spinout, Pearl Street uses AI to streamline renewable energy grid interconnection, addressing one of the most critical bottlenecks in clean energy deployment. This deal reflects a broader shift. Strategic acquirers are prioritizing scalable, software-led climate models that solve infrastructure challenges. It also reinforces the AI-climate nexus as a genuine driver of commercial value, not just a technological add-on.

Climate VC is entering a more mature phase. Hype is giving way to conviction. With fewer short-term players and a more experienced investor base, the market is becoming sharper in its sector focus and clearer in its signals. For limited partners, this presents a more calibrated path to engage—whether to support decarbonization goals, hedge systemic climate risks, unlock regulatory or tax incentives, or gain early exposure to a long-term structural transformation.

Beyond products: Managing climate risk from inception

Early-stage investing isn’t just about finding the next big product, it’s also our job to build durable companies that can withstand shocks, adapt quickly, and scale sustainably in a changing world.

Too often, climate risk is reduced to emissions data. But its real implications run deeper: water and resource scarcity, grid instability, biodiversity loss, infrastructure fragility, and geographic exposure. These risks can affect operations, supply chains, pricing, and even long-term viability.

We’ve developed a structured approach to assessing climate risk across early-stage companies, focusing on real-world vulnerabilities beyond carbon metrics. We evaluate sector exposure, location-specific vulnerabilities, infrastructure dependencies (including AI compute), and potential misalignment between product ambition and operational footprint.

Our latest assessment, with the methodology detailed in our latest report, flagged 10% of companies as facing elevated short-term climate risk. But after factoring in founder-led mitigation strategies already underway, that number dropped to just 3%. This gives us a clearer picture of where to focus support and where resilience is already being built from within.

Climate investing is not only about funding solutions, but also about equipping companies to navigate the world they’re scaling into.

Antler and climate

Our approach is straightforward: build, back, and scale early. With one of the world’s largest early-stage funnels, and proprietary founder access, we capture upside others miss.

We have over 200 active climate-related tech companies in our portfolio currently. We invested in 80 in 2024 alone. Our portfolio spans software, hardware, biology, and infrastructure—addressing climate across sectors. From bioplastics in Vietnam to grid analytics in Norway, autonomous waste sorting in the UK, battery storage in India, animal-free milk in Brazil, and reusable satellite platforms in the US, our portfolio is helping define what climate innovation really looks like.

Number of climate-related portfolio companies backed by Antler each year

We don’t treat climate as a niche, but as the infrastructure of the next economy.

The edge of opportunity

Climate is a system-wide opportunity touching over 70% of global GDP8. For institutional investors, the question isn’t whether to engage, but how early. Will you help shape the future, or buy it later at a premium?

Alpha will not come from crowded Series B rounds or climate-themed ETFs. It is taking shape in pre-product teams rethinking cement chemistry, in engineers designing autonomous microgrids, and in biologists developing carbon-consuming microbes.

The next generation of winners will not mirror the last. They will emerge at the intersection of software and sustainability, often in overlooked markets, solving for resilience, regeneration, and resource efficiency rather than focusing only on emissions.

This is where climate alpha is being built. Investors with proximity to company formation, who help shape the architecture early, are best positioned to capture it.

References:

- Silicon Valley Bank's (SVB) 2025 Future of Climate Tech report

- McKinsey, The Net-Zero Transition: What It Would Cost, What It Could Bring (2022).

- Climate Policy Initiative, State of Climate Finance for Adaptation (2023).

- SVB (2024).

- IEA projections.

- DeepSeek (2024).

- PwC, State of Climate Tech 2024.

- Systemiq and World Bank.

At Antler, we define climate-related technology as innovations that drive positive environmental change across a wide range of sectors, not limited to emissions reduction, by addressing the full spectrum of climate and environmental challenges.

Antler is a global early-stage venture capital firm that backs founders from inception to Series C, with a presence in 26 cities across six continents. Explore www.antler.co to learn more about our portfolio, investment strategy, and global founder residencies.

ANTLER RESIDENCY —LAUNCH YOUR STARTUP

Antler backs exceptional founders to go further, faster.